The Impact of Higher Temperatures on Economic Growth

Federal Reserve Bank of Richmond, August 2018, No. 18-08

Riccardo Colacito, Bridget Hoffmann, Toan Phan and Tim Sablik

What happens to the economy when it gets hot outside? Despite long-standing assumptions that economic damage from rising global temperatures would be limited to the agricultural sector or developing economies, this Economic Brief presents evidence that higher summer temperatures hurt a variety of business sectors in the United States.

June 2018 was the third-warmest on average across the contiguous forty-eight states since record keeping began in 1895, according to the National Oceanic and Atmospheric Administration (NOAA). Only 1933 and 2016 saw hotter starts to the summer.

Climate scientists project that average global temperatures will rise over the coming decades, which could have a variety of environmental impacts. But what impact would higher temperatures have on the economy? To date, studies of this question have largely focused on developing countries, under the assumption that those countries are more exposed to the effects of higher temperatures. The economy in developing countries is often more reliant on agriculture or other outdoor activities, and those countries have fewer resources to devote to mitigating the effects of heat through technologies such as air conditioning. Indeed, researchers have found that higher temperatures have significant negative effects on the economic growth of developing nations.1

In the case of developed countries, such as the United States, researchers have focused largely on measuring the impact of warming on outdoor economic activities, such as agriculture.2 Since these sectors make up a relatively small share of the U.S. economy, it has generally been assumed that the economic effects of global warming for the United States would be relatively small. As Nobel prize winning economist Thomas Schelling observed in a 1992 article, “Today very little of our gross domestic product is produced outdoors, susceptible to climate.”3

However, research by three authors of this Economic Brief (Colacito, Hoffmann, and Phan) finds that the consequences of higher temperatures on the U.S. economy may be more widespread than previously thought. By examining changes in temperature by season and across states, they find evidence that rising temperatures could reduce overall growth of U.S. economic output by as much as one-third by 2100.4

Warming across Seasons and across States

Attempting to measure the relationship between temperature and growth by looking at the whole United States can hide important variations. Some parts of the country have higher average temperatures. Further increasing temperatures in those areas may be more harmful than rising temperatures in parts of the country that are generally cooler. In fact, higher temperatures in colder regions or during colder seasons actually may have positive effects on economic activity because extreme cold can be as much an impediment to certain activities as extreme heat.

Highlighting the importance of these seasonal and regional variations, Colacito, Hoffmann, and Phan find no statistically significant relationship between temperature and economic growth when looking across the whole United States. But measuring the impact of temperature in different seasons and across individual states yields different results. The authors take the average of daily weather observations from NOAA for each season for 1957–2012. They define each season as a quarter of the calendar year: January through March is winter, April through June is spring, July through September is summer, and October through December is fall. This definition aligns the temperature data with the quarterly periods used for economic data.

Colacito, Hoffmann, and Phan find that temperature increases in the summer are associated with a decline in gross state product (GSP), which is the value added in production by the labor and capital of all industries in a given state. On average, each 1˚F increase in the mean summer temperature reduces the annual GSP growth rate by 0.154 percentage points. A reduction in the growth rate, as opposed to the level of economic output, has important implications for the impact of temperature changes in the long run. Changes to the growth rate compound over time and, as a result, are more lasting.

As theory would suggest, Colacito, Hoffmann, and Phan also find that higher temperatures during the colder fall months have a positive effect on growth. On average, each 1˚F increase in the mean fall temperature increases the annual GSP growth rate by 0.102 percentage points. This finding is smaller and less statistically robust than their finding for the summer effect, but it may help explain why temperature changes do not appear to have a significant effect on growth when averaged across the whole year and across the whole country: the effects in the summer and fall partly offset. The authors do not find any significant effects for temperature increases in the spring or winter.

Measuring the impact of temperature changes on states as opposed to the country as a whole also reveals significant variations. Colacito, Hoffmann, and Phan divide the country into four regions — North, South, Midwest, and West — using classifications from the U.S. Census Bureau. Average temperatures are highest in the South, and the authors find that the economies of southern states are the most sensitive to changes in summer and fall temperatures. Further investigation shows that this effect is not driven by a larger role of agriculture in southern states. In fact, the authors find that the economic effects of temperature are widespread across a variety of industries.

Rising Temperatures Hurt Many Industries

One might easily presume that higher temperatures would only affect agriculture. But in fact, studies have documented the effects of extreme temperatures on other industries. For example, temperatures above 90˚F have been found to reduce production at automobile manufacturing plants in the United States.5 Another study published by the Chicago Fed found that severe winter weather has a significant, albeit short-lived and generally small, negative effect on a variety of industries.6 In line with these findings, Colacito, Hoffmann, and Phan find that higher temperatures in the summer have a negative effect on labor productivity generally, while higher fall temperatures have a positive impact.

Losses in labor productivity have the potential to impact a wide range of industries, which is exactly what Colacito, Hoffmann, and Phan find. (Figure 1 shows results for 1998–2012.) The two largest sectors of the U.S. economy — services and FIRE (finance, insurance, and real estate) — make up half of national GDP and are both hurt by higher summer temperatures. More housing transactions take place in the spring and summer, perhaps because house shopping involves travel and outdoor activity. As temperatures rise, potential homebuyers may tend to stay inside, which could help explain the finding that higher summer temperatures negatively impact the real estate sector.7

Studies also have documented that high temperatures negatively affect health, resulting in increased hospitalizations.8 Colacito, Hoffmann, and Phan hypothesize that this connection may explain the finding that higher summer temperatures have a substantial impact on the insurance sector. As health outcomes worsen, insurers would face increased claims. Overall, the authors find that a 1˚F increase in temperature is associated with a 1.30 percentage point decline in output growth for the insurance sector.

As expected, the authors also find that higher summer temperatures have a large negative effect on agriculture, forestry, and fishing. Although this sector accounts for only about 1 percent of national GDP, losses in this area may spill over to other sectors of the economy, such as retail food services. Higher summer temperatures do have a positive effect on some industries, including utilities and mining, benefits that may stem from increased energy consumption during hotter days.

Looking Ahead

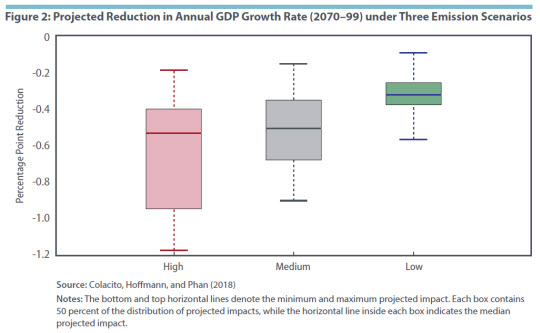

Although the effects estimated by Colacito, Hoffmann, and Phan are robust, they are also small in the short term. Over a longer horizon, however, the impact on GDP growth rates may be substantial. The authors study the effects of rising temperatures in the future using projections for average temperatures in the United States over the years 2070–99.9 These estimates use three different scenarios of future greenhouse gas emissions (high, medium, and low) by the Intergovernmental Panel on Climate Change. The authors apply these estimates to their analysis, assuming that states do not make any changes to adapt to or mitigate the effects of higher temperatures and that the effects of temperature on economic growth that they found in their state-by-state analysis do not change.

Under the low-emissions scenario, the authors estimate that rising temperatures would reduce the growth rate of GDP by 0.2 to 0.4 percentage points from 2070 through 2099, or as much as 10 percent of the historical average annual growth rate of 4 percent. Under the high-emissions scenario, rising temperatures could reduce the growth rate by up to 1.2 percentage point, or roughly one-third of the historical average annual GDP growth rate. (See Figure 2.) The authors note that these estimates should be “interpreted with caution,” since future adaptations to changing temperatures may mute the long-run effects they calculate.

While the impact of future climate adaptations is unknown, Colacito, Hoffmann, and Phan do examine whether more widespread climate adaptation within their sample period may have reduced the impact of temperature on growth. In fact, they find that the negative impact of higher summer temperatures is larger and still statistically significant after 1990, while the positive fall effect becomes smaller and statistically indistinguishable from zero. Thus, if anything, they find that the negative impact of temperature increases on GDP growth has become more pronounced in recent decades despite advances in adaptive measures.

Overall, these findings suggest that rising temperatures in the future could hamper economic growth in a variety of industries even in developed nations such as the United States.

Riccardo Colacito is an associate professor of finance and economics at the University of North Carolina, Chapel Hill, and Bridget Hoffmann is an economist in the Research Department at the Inter-American Development Bank. Toan Phan is an economist and Tim Sablik is an economics writer in the Research Department at the Federal Reserve Bank of Richmond.

1John Luke Gallup, Jeffrey D. Sachs, and Andrew D. Mellinger, “Geography and Economic Development ,” International Regional Science Review, August 1999, vol. 22, no. 2, pp. 179–232; William D. Nordhaus, “Geography and Macroeconomics: New Data and New Findings,” Proceedings of the National Academy of Sciences of the United States of America, March 2006, vol. 103, no. 10, pp. 3510–3517; Melissa Dell, Benjamin F. Jones, and Benjamin A. Olken, “Temperature Shocks and Economic Growth: Evidence from the Last Half Century,” American Economic Journal: Macroeconomics, July 2012, vol. 4, no. 3, pp. 66–95.

,” International Regional Science Review, August 1999, vol. 22, no. 2, pp. 179–232; William D. Nordhaus, “Geography and Macroeconomics: New Data and New Findings,” Proceedings of the National Academy of Sciences of the United States of America, March 2006, vol. 103, no. 10, pp. 3510–3517; Melissa Dell, Benjamin F. Jones, and Benjamin A. Olken, “Temperature Shocks and Economic Growth: Evidence from the Last Half Century,” American Economic Journal: Macroeconomics, July 2012, vol. 4, no. 3, pp. 66–95.

2See, for example, Marshall Burke and Kyle Emerick, “Adaptation to Climate Change: Evidence from U.S. Agriculture,” American Economic Journal: Economic Policy, August 2016, vol. 8, no. 3, pp. 106–140.

3Thomas C. Schelling, “Some Economics of Global Warming,” American Economic Review, March 1992, vol. 82, no. 1, pp. 1–14.

4Riccardo Colacito, Bridget Hoffmann, and Toan Phan, “Temperature and Growth: A Panel Analysis of the United States,” Federal Reserve Bank of Richmond Working Paper No. 18-09, March 2018.

5Gerard P. Cachon, Santiago Gallino, and Marcelo Olivares, “Severe Weather and Automobile Assembly Productivity,” Columbia Business School Research Paper No. 12/37, December 2012.

6Justin Bloesch and François Gourio, “The Effect of Winter Weather on U.S. Economic Activity,” Federal Reserve Bank of Chicago Economic Perspectives, First Quarter 2015, vol. 39, no. 1, pp. 1–20.

7L. Rachel Ngai and Silvana Tenreyro, “Hot and Cold Seasons in the Housing Market,” American Economic Review, December 2014, vol. 104, no. 12, pp. 3991–4026.

8See, for example, Ekta Choudhary and Ambarish Vaidyanathan, “Heat Stress Illness Hospitalizations — Environmental Public Health Tracking Program, 20 States, 2001–2010,” Morbidity and Mortality Weekly Report, Surveillance Summaries, December 12, 2014, vol. 63, no. 13.

9Temperature estimates come from Evan H. Girvetz, Chris Zganjar, George T. Raber, Edwin P. Maurer, Peter Kareiva, and Joshua J. Lawler, “Applied Climate-Change Analysis: The Climate Wizard Tool,” PLoS One, December 2009, vol. 4, no. 12, e8320.