Source: Len Keifer

To hear an audio spoken word version of this post, click here.

Alas, the bubble callers are out and about, this time, calling a new bubble in housing. I will spare you my usual lecture on denominator blindness, and point out this is not what it appears.

Start with last week’s WSJ article noting “there are more real-estate agents than homes for sale in the U.S.” We can reach that point in one of two ways: either lots of people go into real estate as a side hustle (its super easy to become an agent in most states – some don’t even have agent tests). Or, there could be very few homes for sale.

The USA seems to have both circumstances taking place today. As the chart above shows, we are at record low inventory for sale. That chart is the handiwork of Len Keifer, the Deputy Chief Economist at Freddie Mac (MiB here).

As the chart above shows, we are at record low inventory for sale. That chart is the handiwork of Len Keifer, the Deputy Chief Economist at Freddie Mac (MiB here).

As we learned in Economics 101, too little Supply at constant Demand will naturally send prices higher. That’s one side of the equation.

We have also seen demand for suburban homes rise over the past year. During the pandemic, lots of people were stuck in small apartments, paying high urban rents but enjoying none of the usual urban amenities that attracted them to the city in the first place.

What followed: Anyone who could afford to head to the ‘burbs during the pandemic lockdown did so — for the space, the less contagious environment, the ability to both work- and school-from home, and generally to not want to murder other members of your own family.

In a normal market, it does not take much of a shift to create an imbalance. Housing here is both too little supply and too much demand; these look like temporary issues, not a longer lasting condition.

Another factor: Getting approved for a Mortgage is much harder today — probably too hard – than in the past.

Housing over the 2001-2007 period was a very different environment then today. The Supply/Demand balance was shifted dramatically when financiers radically changed what was needed to qualify for a mortgage. That created an extra 5 million new buyers coming into the market. That’s what happens when you remove qualifiers like a FICO score, job history, even income!

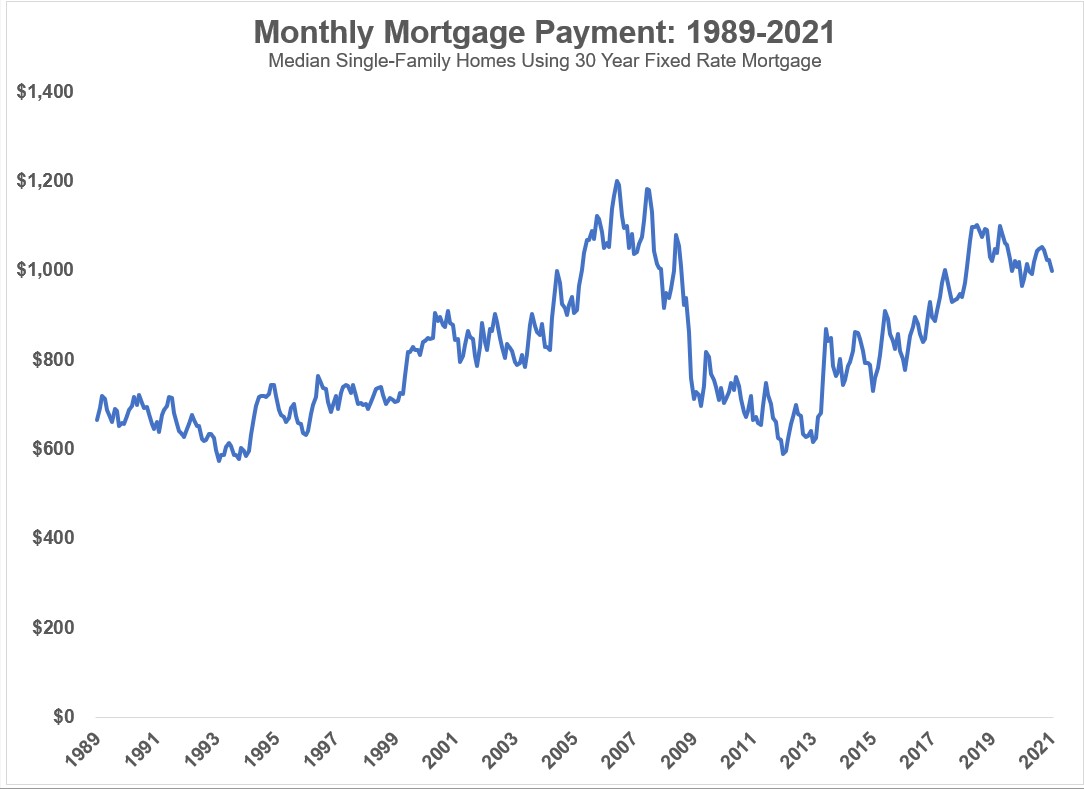

My colleague Ben Carlson does a nice job explaining why prices out of context can be misleading: Home prices are merely one part of the equation. Given the 15- or 30-year payoff, its the monthly costs of servicing the mortgage that matter the most.

Here is Ben:

Mortgage rates were more than 10% in 1989. So while prices were far lower in the past, borrowing rates were much higher.

Taking the median sales price and applying the prevailing 30 year fixed mortgage rate (after accounting for a 20% down payment) shows a different story when it comes to monthly payments:

Source: A Wealth of Common Sense

Ben adds “the wave of millennials buying means demographics is going to be a huge force in driving the next 5-7 years at least.” In other words, future housing demand is structural, not this speculative.

If you have been reading me long enough you may recall I saw that one coming in advance and yelled long and loud about it. I see nothing here remotely like the lead up to 2008-09.

Add all of these factors up, and it does not look like a housing bubble to me. There are numerous factors that go into real estate prices, but you always have to be cautious about anything involving ratios. I won’t say it is impossible for this to eventually morph into a housing bubble, but — at least so far — it looks nothing like housing bubbles of the past.

UPDATE June 16, 2021

The WSJ: “U.S. Housing Market Needs 5.5 Million More Units, Says New Report”