To hear an audio spoken word version of this post, click here.

As 2021 drew to a close, the Omicron variant was surging. Infections and hospitalizations had spiked to their highest levels, and a budding sense of normalcy and economic re-opening ground to a halt. We were lucky that Omicron was not especially dangerous to the vaccinated and boosted (although Long Covid remains a concern). Mask mandates are ending just about everywhere, today. The pandemic seems to be entering its endemic phase, with enough preventative measures and viable treatments to turn a deadly scourge into a more manageable virus.

Instead of celebrating this, we are instead confronted with a daily parade of televised war crimes.

This has shifted our attention away from re-opening, and towards the Russian invasion of Ukraine. It is likely dominating your focus these days (we discussed the impact last week), but consider for just a moment the ongoing economic recovery in the United States and the rest of the world.

But for Putin’s folly, we would be discussing a 5+% GDP, blowout jobs report, unemployment falling to pre-pandemic levels, rising retail and housing sales, along with a substantial increase in prices.

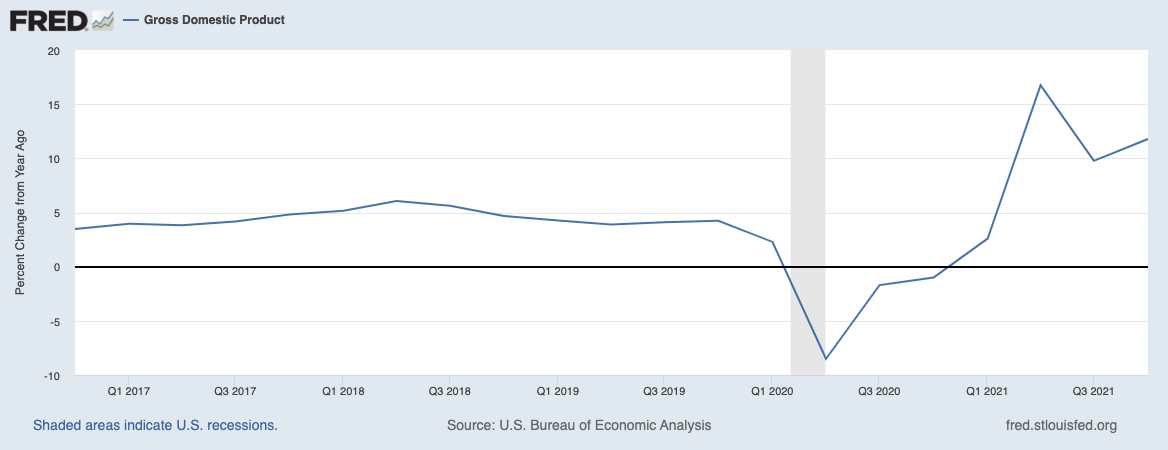

Prior to the initiation of hostilities, there were 5 distinct phases evident in the U.S. economy:

1. Soft recovery from the Great Financial Crisis, which began accelerating in the mid-2010s

2. February/March 2020 collapse into the pandemic, making lows in Q2 2020

3. Reversal from that low rallying to Q2 2021 highs

4. Delta/Omicron variant pullback Q3-Q4 of 2021

5. New economic increases ~Q1 2022

It is probable that but for the invasion of Ukraine by Russia, Global GDP would be accelerating further, even in the face of rising rates and (transitory?) inflation.

There are endless unknowns confronting the world today, but for investors, the key issue is which of these global events will be the prime driver for the rest of 2022? I hope that we see a cessation of hostilities sooner than later, and expect the global economy to work past the war.

We can ask questions: How is Russia is going to act in Ukraine, in Europe, and in the global marketplace? What will key players in the energy space like Saudi Arabia and U.S. Frackers do in response to rising prices and falling Russian Oil/Gas supplies? How will the Federal Reserve alters its rate-hiking plans (if at all)? How will global sentiment develop as ongoing Russian aggression becomes more brutal? How will U.S. consumers behave in the face of rising prices, and increasing geopolitical uncertainty?

It is too easy to think of the world as having grown more complex and harsher over your lifetime: Various wars (Viet Nam to Iraq to Ukraine) scandals, (Watergate, Clinton Impeachment, Trump impeachments) September 11th attacks, the financial crisis, Covid pandemic, the January 6th insurrection, and whatever the hell comes next. I remain unsure as to whether the world is growing harsher, or if we are merely becoming less naive about it. Maybe with ubiquitous cameras-phones in everybody’s pockets, we are less able to remain naive about the world.

I wish we were discussing a red hot economy and the corresponding stock market in the context of inflation and rates; instead, this debate has evolved into an ongoing discussion of the realignment of Western Liberal Democracies and the impact of the hostilities on prices of oil wheat nickel and rare-earth minerals, and the staggering human toll the war is inflicting.

I long wistfully for the simpler days of debating whether inflation is transitory or not . . .

Previously:

Exiting Russia (March 3, 2022)

War Impacts Stocks Less than You Think (March 2, 2022)

History Shows War Shocks Have a Modest Impact on Equities (BusinessWeek, March 2, 2022)

MSCI: Russia’s Stock Market is “Uninvestable” (February 28, 2022)

How Geopolitics Impacts Markets: 1941-2021 (February 25, 2022)

Which Matters More to Markets, Omicron or Ukraine? (February 22, 2022)

click for audio