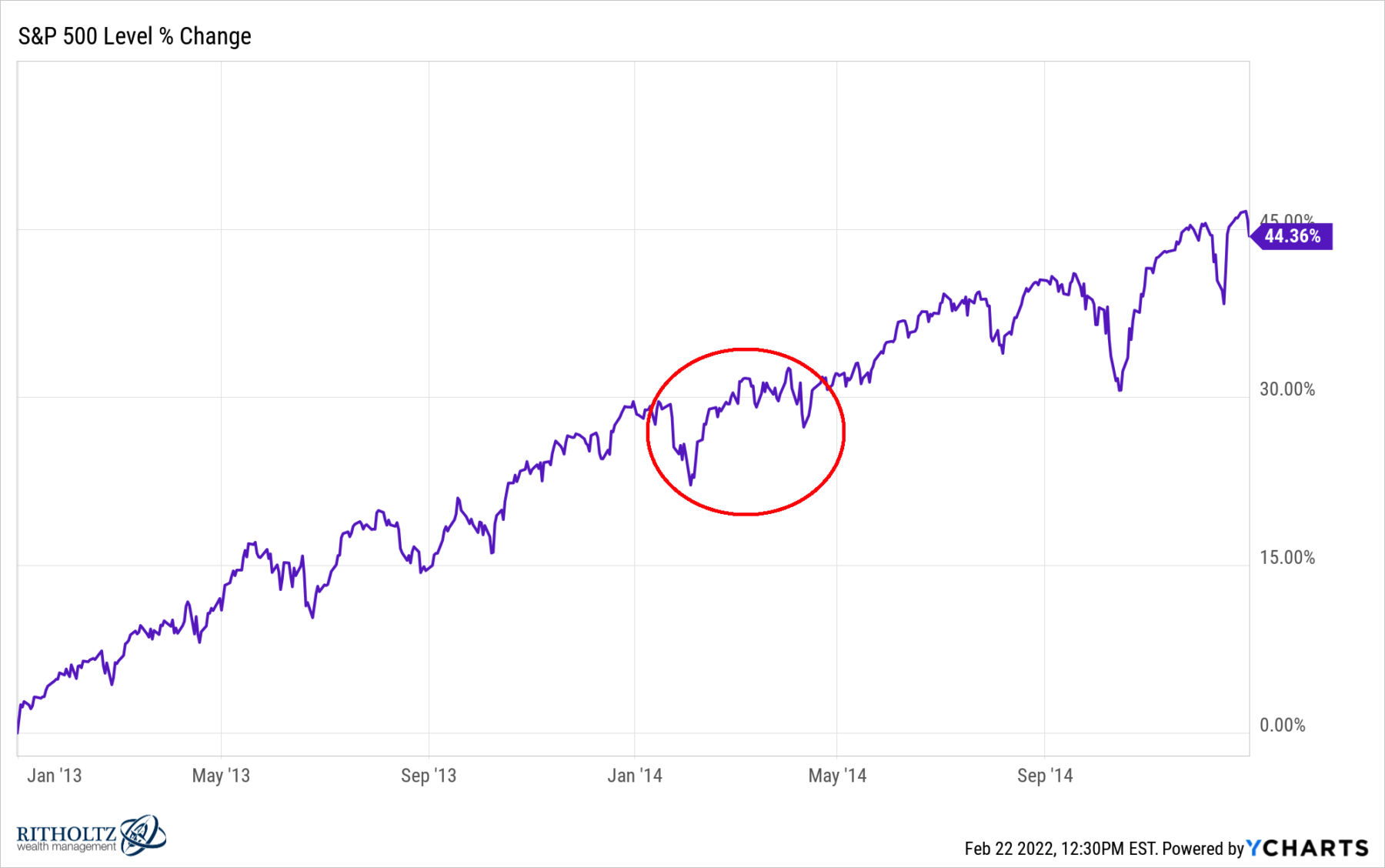

2014 S&P 500; showing Russian Annexation of Crimea (circled in red)

Has it really been two years since my last vacation? I bet you also miss the opportunity to unplug, recharge your batteries, and spend a week just doing nothing but hanging out, relaxing, thinking – and drinking too many mojitos.

Omicron looked frightful a month before we left, but the numbers crashed hard here and abroad, and so off we went. When 70% of your economy is dependent on tourism, you make sure your protocols make people comfortable that they won’t test positive and get stuck on your island for another 10 days. There are no tribal arguments about masking or vaccines or boosters – no Karens causing grief in a supermarket. If you want to fly down to our island, show proof of vaccination and a negative COVID test within three days of your flight – or stay home.

Omicron looked frightful a month before we left, but the numbers crashed hard here and abroad, and so off we went. When 70% of your economy is dependent on tourism, you make sure your protocols make people comfortable that they won’t test positive and get stuck on your island for another 10 days. There are no tribal arguments about masking or vaccines or boosters – no Karens causing grief in a supermarket. If you want to fly down to our island, show proof of vaccination and a negative COVID test within three days of your flight – or stay home.

We checked into our hotel room, shed the masks, and most of our worries about catching COVID. The return flight was similarly strict – a COVID test the day before we left administered by a medical professional (no home tests allowed).

48 hours after my return, Russia violated Ukraine’s borders.

Looking at the market’s reaction, I am trying to guess what is already priced in; but this exercise raises an interesting question:

Which is of greater import, Russian aggression or the beginning of the end of COVID?

We have two historical reference points: The Russian Federation’s annexation of Crimea in February and March 2014 (See chart at top), and the apparent end of Covid Delta and Covid Omicron (see chart below).

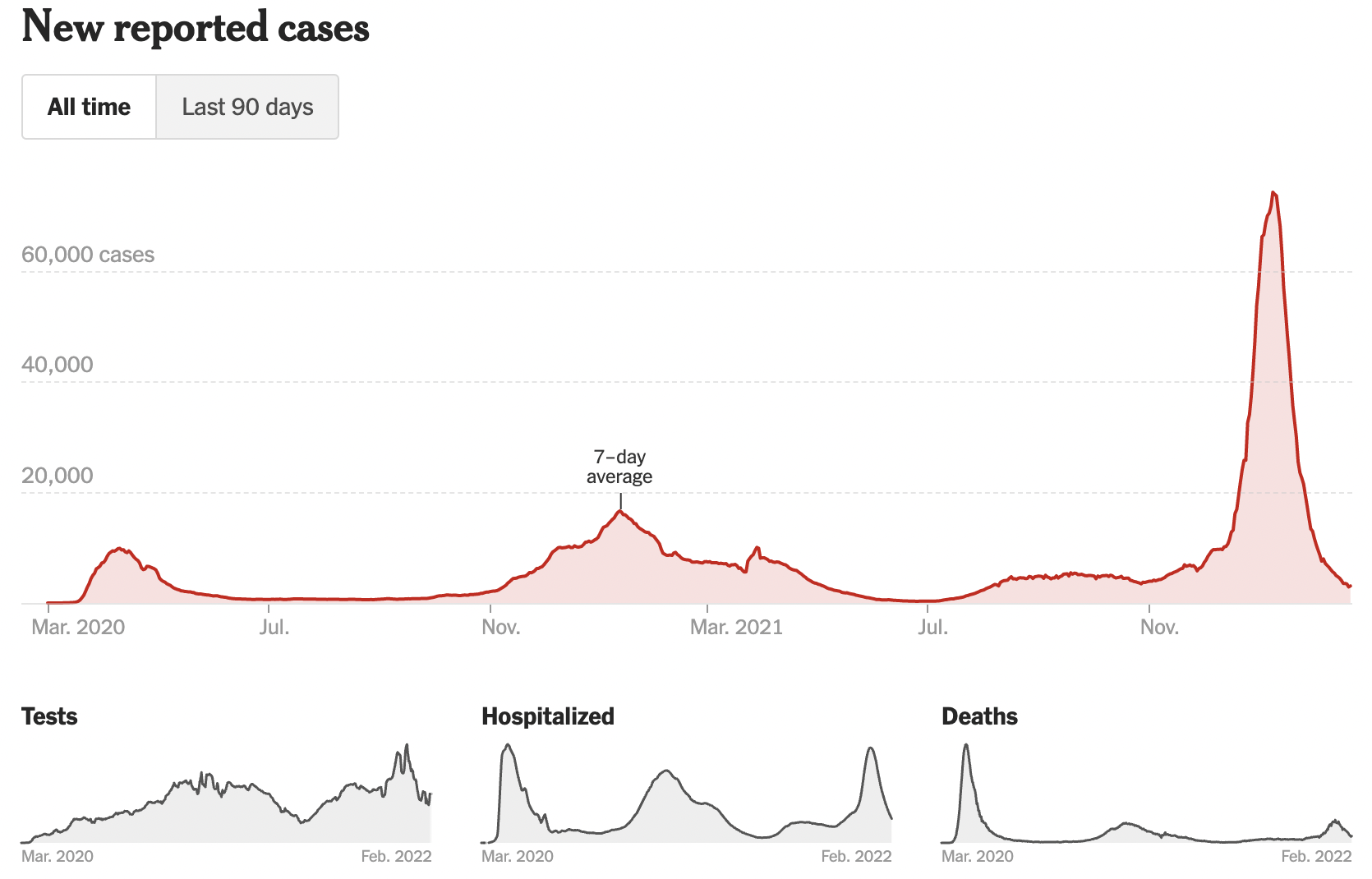

The World Health Organization (WHO) indicated in June 2021 that the Delta variant was becoming the dominant strain globally. The Omicron variant was first reported to the World Health Organization (WHO) from South Africa on November 24, 2021.

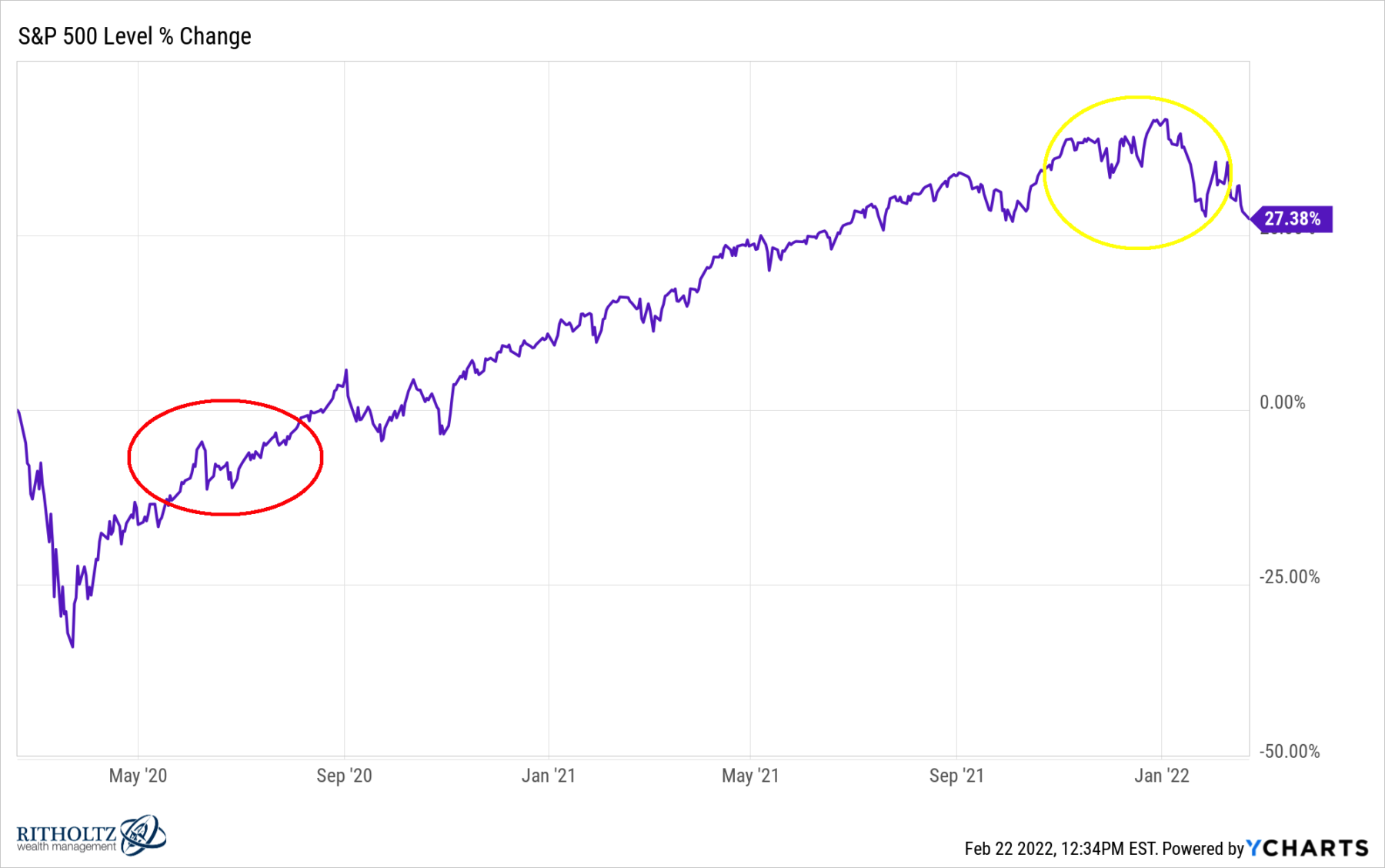

2020-21 S&P 500; showing Delta variant (circled in red) and Omicvron variant (circled in yellow)

I will spare you my usual exposition here on narrative fallacy and hindsight bias and our tendency to try and explain what is more or less random market action by our experiences to explain what just happened.

Suffice it to say that you can always confabulate an explanation based on what occurred with your ex post facto knowledge.

The annexation of breakaway states — assuming it doesn’t become a full-fledged World War — does not appear to be a substantial threat to markets. And offsetting the geopolitical turmoil is a genuine sense that Omicron is in full retreat, allowing the economy to once again attempt to reopen (assuming no further highly contagious variants show up).

That is a lot of big ifs: Less than a full-blown invasion, and no more dangerous variants are certainly possible. But so too is a messy shooting war and even more contagious variants, some of which might be potentially more dangerous than Delta/Omicron.

Markets are off as of this writing about a percent and change.

To me, the bigger question is the above-average returns of about 13% annually the markets have enjoyed the past decade (including the 34% COVID crash).

To me, the bigger question is the above-average returns of about 13% annually the markets have enjoyed the past decade (including the 34% COVID crash).

That sort of outperformance tends to eventually mean revert — and that’s before we even talk about last year’s nearly 28% gains in the S&P 500. It is rational to expect to see returns towards historical gains of about 8% per year.

You should have no problem with 2022 being in the -5% to +5% range, give or take a little. Theoretically, rates should begin normalizing, supply chains untangle, inflation begins to ebb as the fiscal stimulus begins to fade, and perhaps, hopefully, reopening finally sticks.

I don’t know what comes next, but we can all hope for a return to normality after the past 2 years of mayhem. Whatever your thoughts are for next few quarters, I see more sunshine than rain over the next few years . . .

Update: February 24, 2022

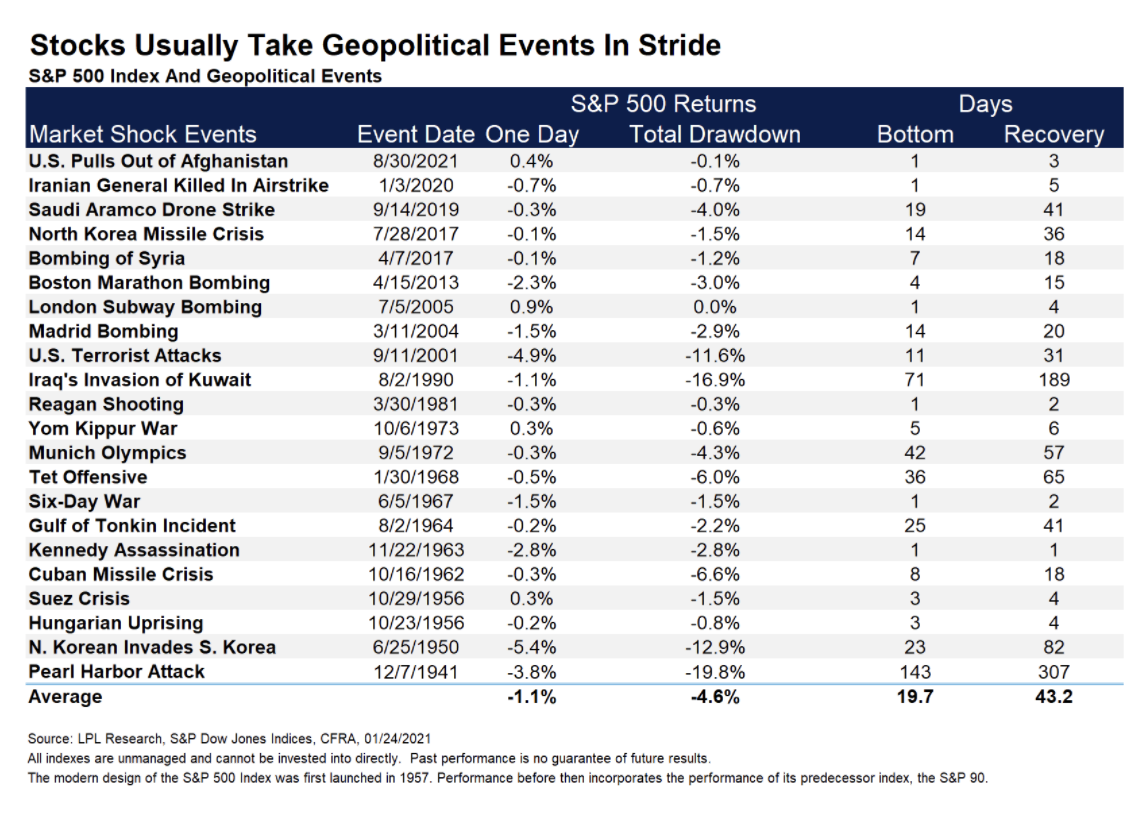

Josh points to LPL/Ryan Detrick’s table showing the impact of geopolitics on markets.

Previously:

Explaining the Correction, with Perfect Hindsight (October 15, 2018)

Choose Your Market Narrative (November 5, 2020)

End of the Secular Bull? Not So Fast (April 3, 2020)

Living Through a Crash (January 14, 2022)

What is the Market Up To? (January 24, 2022)