One of my favorite ways to contextualize market trends is to divide long periods of time into secular bull and bear markets.

When we look at the past century, we can see decades-long eras where the economy is generally robust, supporting markets trending higher, with expanding multiples. We call these eras Secular Bull Markets. The best examples are 1946-66, 1982-2000, and 2013 forward.

The alternate periods of time are Secular Bear Markets: The economy is fraught with weakness, poor consumer spending, and negative job growth. Corporate revenues and earnings are weak; equity prices go sideways, with vicious rallies and sell-offs common. Investors are decreasingly willing to pay the same amount for a dollar of earnings.

Regardless of which of these secular market periods we happen to be in, no market goes straight up or down forever. Markets will move in the opposite direction of the dominant trend. During secular bull markets, we get cyclical bears; during secular bear markets, we get cyclical rallies.

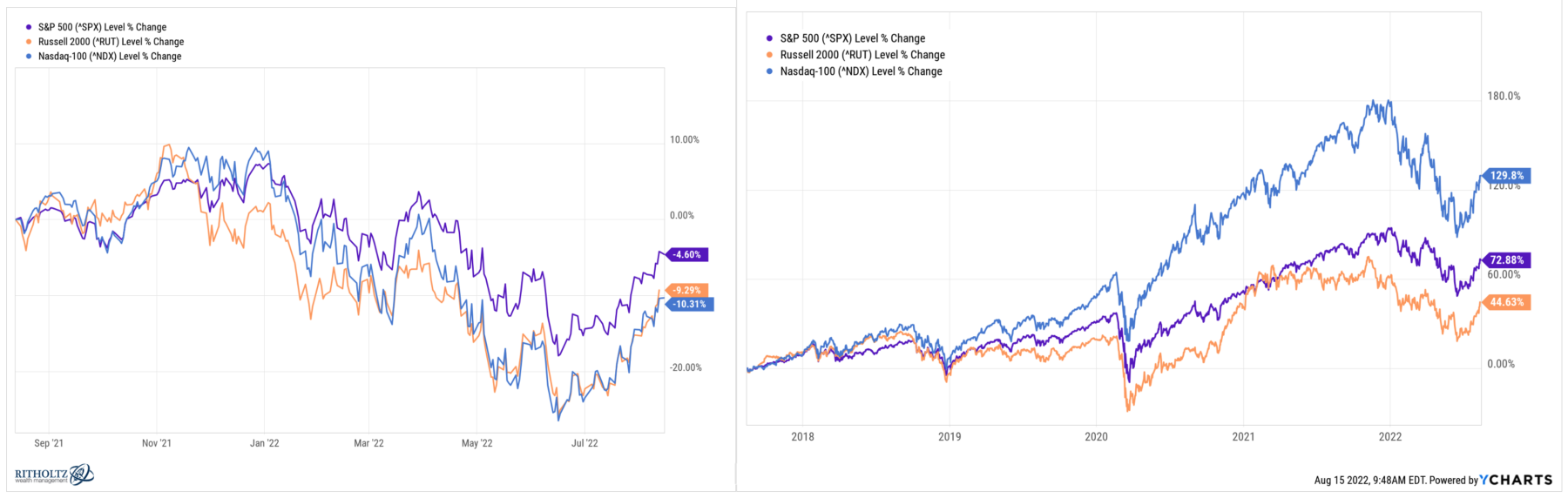

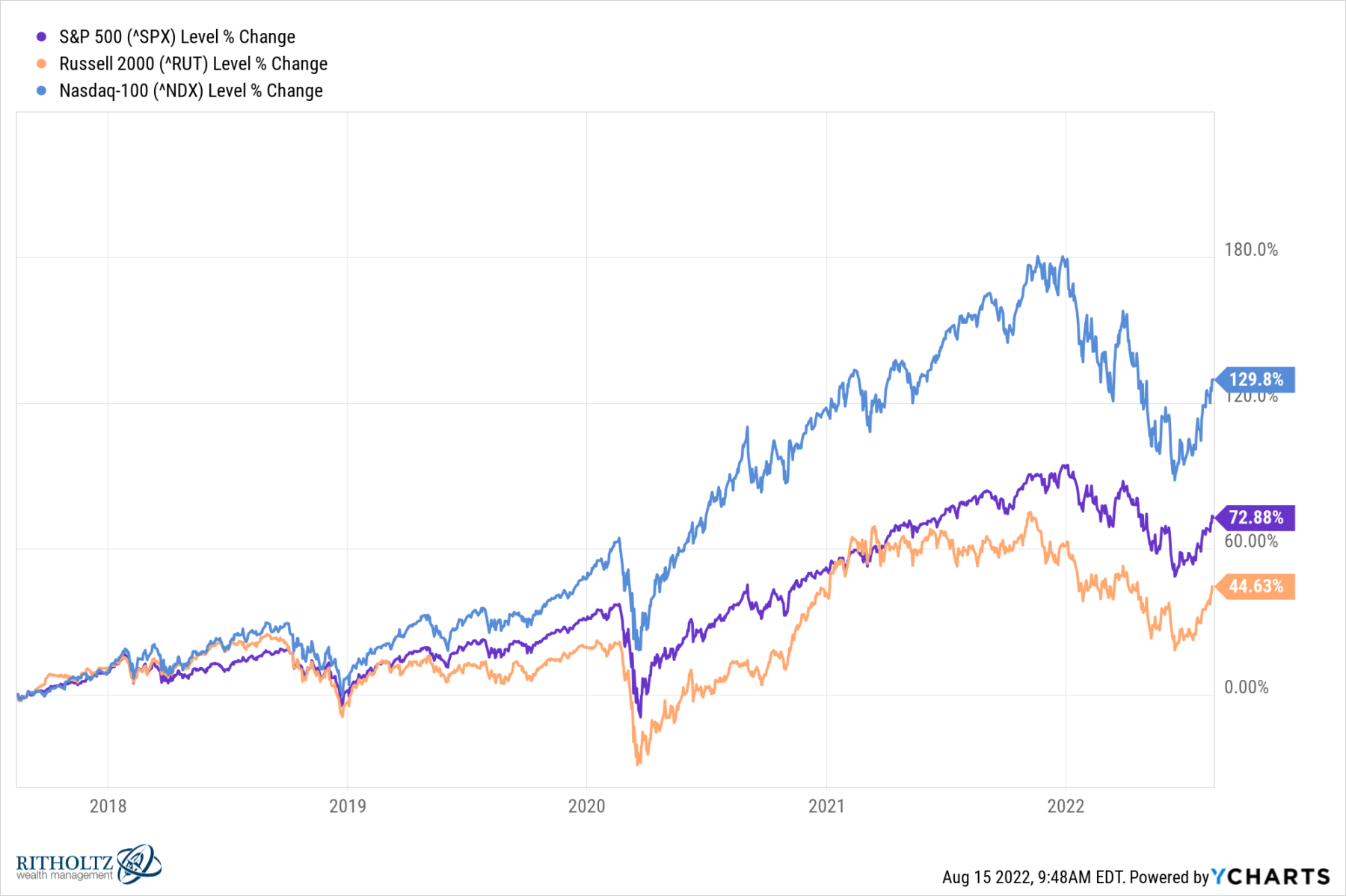

Some people are describing the current move off of the June lows as a bear market rally. for this to be the case two things must have happened: 1) The secular bull market that began in 2013 has ended, and 2) We are now in a new secular bear market.1

If you believe that the 2013 secular bull market is still in effect then it is reasonable to make the claim that the first half sell-off was a countertrend cyclical bear within the context of a secular bull. This is supported generally by economic strength in the labor market, strong consumer spending, and record high corporate profits.

The counterargument is the spike in inflation has changed the dynamic of the economy. We should expect to see slowing industrial production, weakening consumer spending, increased layoffs, and rising unemployment as the Fed tightens to kill inflation.

Typically, secular bull and bear markets are best identified after the fact – something that allows precision but is useless for investors. In real-time, you have to make your assumptions and place your bets.2

The question that determines how traders might want to position themselves this simply which sort of counter-trend rally is this?

Cyclical rally within a Secular Bear?

Or Recovery from a Bear Cycle within a Secular Bull?

Perhaps we can glean some insight from Bryan Jordan, Deputy Chief Economist at Nationwide. Since the June lows, we have seen 4 consecutive weeks of market gains (+16.7%) which recovered more than half of the YTD losses.

Jordan asks the question “How does the current rally stack up?” Taking a contrarian stance, he notes “The uptrend is still widely expected to fizzle — consider the prevalence of the phrase “bear market rally” of late.”

But he also observes a key historical measure:

“Note that it has already outstripped the biggest countertrend gains in eight out of the last ten bear markets. The only bear market rallies in the last seven decades stronger than the rise of the last two months were increases of 19.0%, 21.2%, and 20.7%, respectively, during the 2000-02 downturn and a 24.2% upturn near the tail end of the 2007-09 cycle. Every other rally of this magnitude that began during these periods represented the start of a new bull market.”

We won’t know for sure until after the fact but it certainly hurt helps us to understand this context better.3

Previously:

End of the Secular Bull? Not So Fast (April 3, 2020)

Bull Markets & P/E Multiple Expansion (June 22, 2018)

Bull Markets Can’t Start Until Bear Markets End (March 9, 2018)

Redefining Bull and Bear Markets (August 14, 2017)

Are We in A Secular Bull Market? (November 4, 2016)

___________________

1. We have discussed previously why the pandemic externality was not an end to the prior secular bull market. See this. that viewpoint was affirmed by the subsequent move in 2020 and 2021.

2. Unless you are a buy and hold investor as we are which means that you ride out the ups and downs of the counter-trend rallies in order to benefit from the longer-term secular trend.

3. I would be doing a disservice to Jordan if I omitted his caveats:

“There are, of course, fundamental reasons to remain cautious. The Federal Reserve is still aggressively tightening monetary policy and, as a result, the risk of an eventual recession is still on the climb. As noted in this space on several occasions, however, the market has already priced in a fairly negative outcome. The S&P was down by 23.6% from peak in the late spring and is still off by 10.9% even after the rally of recent weeks. Historically, the index has fallen by an average of just 7.6% in pre-recessionary periods.”