Last week, I mentioned the quarterly conference calls I do for clients of RWM, which led to a broad discussion of Sentiment. I want to briefly discuss the fiscal regime change table I created for that call (above).

The TLDR: For the past few decades, the United States’ economic policy has been one primarily driven by ultra-low rates. Beginning under Alan Greenspan, continuing through the terms of Ben Bernanke, Janet Yellen and now Jay Powell, low rates ruled everything around me.

There is a longer discussion to be had on how Zero Interest Rate Policy (ZIRP) impacted assets priced in dollars or credit, wealth inequality, and the rise of populism.1 The bottom line is the primarily monetary (not fiscal) stimulus responses to calamities such as the September 11th terror attacks, or the Great Financial Crisis had unanticipated consequences.

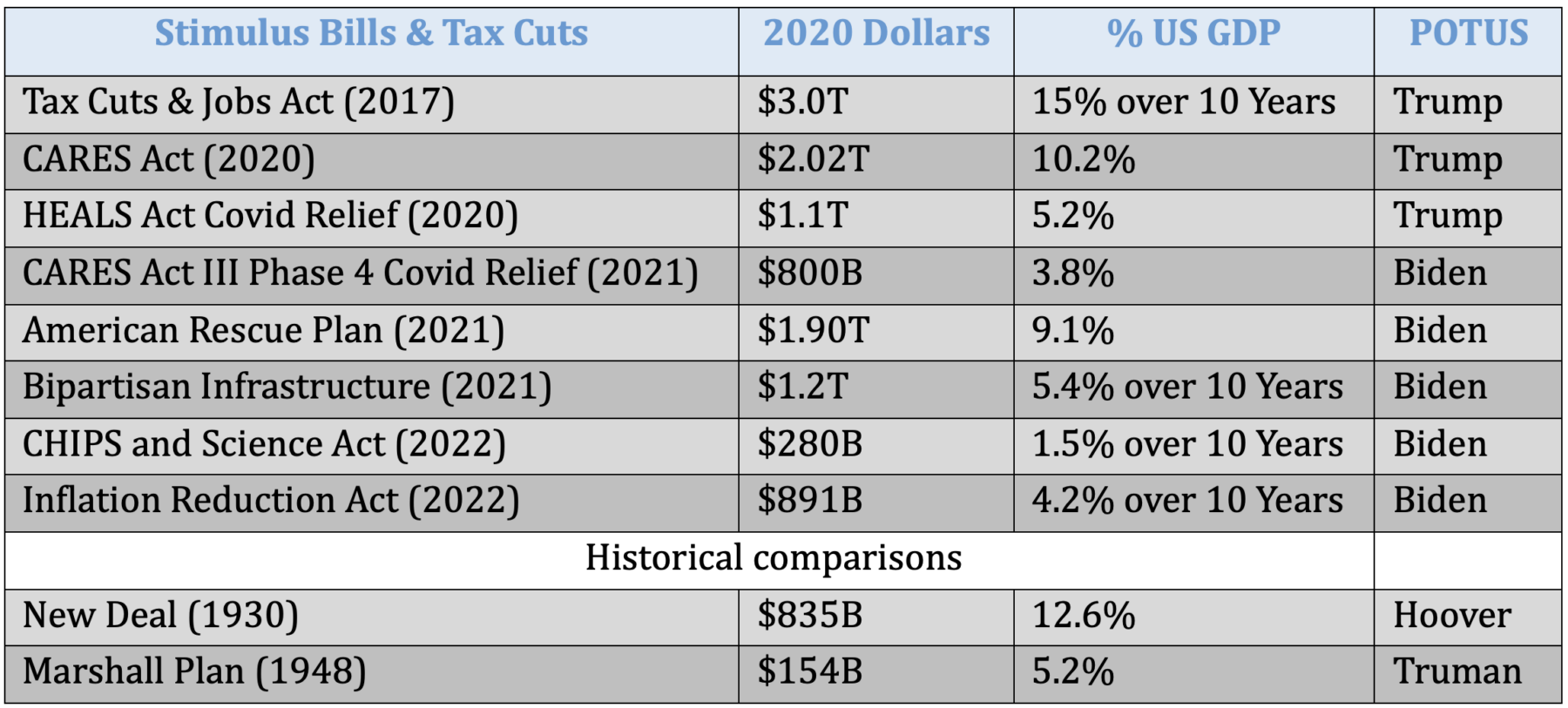

That began to change under President Trump. The Tax Cuts & Jobs Act of 2017 (TCJA) was ~$3 trillion spread out across a decade. It was the biggest fiscal stimulus to come along for some time, and while it was biased towards the upper quarter of the economic strata, it was not thought of broadly in the way we typically consider fiscal stimulus.

Missing its fiscal component was a significant economic misunderstanding.

Then came Covid-19. The CARES Act 1 (2020) at ~10% of GDP, was the largest fiscal stimulus since the Great Depression. It was followed by the 2nd CARES Act, which added nearly another trillion dollars of stimulus. The three of these had a massive stimulatory impact.

Then President Biden came into office; he passed the 3rd CARES Act, the American Rescue Plan, the Bipartisan Infrastructure Bill, the Chips Act, and the Inflation Reduction Act. (Data in the table are totals, but nearly half of those allocations were new money 2). Regardless it was another trillion and a half dollars in immediate stimulus and a few trillion dollars more spread out over 10 years.

At the same time, federal funds rates went from zero to over 5%. The impact on stocks and bonds was unmistakable.

The 2010s were a decade of monetary stimulus that saw equity markets gain 14% annually. Free money! At least, cheap capital, low-cost financing for consumer and commercial purchases, all of which led to higher corporate profits.

It’s very reasonable to presume that more expensive money means higher costs of financing those consumer and commercial purchases; this will probably crimp total retail sales, and could negatively impact corporate profits (eventually).

Hence, you should lower your expectations for future equity gains in the era following ZIRP and QE. If we were getting 12-14% previously, then the 2020s should expect something closer to 5-7% in equity returns.

But concurrent with that is the fixed income portion of your portfolios. I’ll spend more time in a future post detailing why “Cash is no longer trash,” but the bottom line is much of what you lose on the equity side, you gain on the fixed income side. This bodes well for those looking for income, who invest via a 60/40 portfolio, or are otherwise lower-risk investors.

Most of what takes place in the day-to-day world of markets is noisy and meaningless; but the shift from monetary to fiscal stimulus is very, very significant.

Investors would do well in paying attention to this regime change.

Update: October 27, 2023

Here is the discussion about cash/fixed income:

Previously:

The Greatest Missed Opportunity of Our Lifetimes (October 23, 2023)

What Else Might be Driving Sentiment? (October 19, 2023)

Farewell, TINA (September 28, 2022)

__________

1. We will save that for another post…

2. I explained during the call that much of those dollars had been already allocated in other bills and were consolidated under each of these pieces of legislation. Regardless, it was still trillions in fiscal stimulus.