Before yesterday’s FOMC meeting, I reiterated my view from July 2023 that this hiking cycle was – or at least should be – over.

The Narrative bias driving commentary today is that this sudden bullishness is the market sussing out the last hike. But this after-the-fact story does not resonate as truth with me, as it looks more like the 10% market correction of October 2023 has ended. Future discounting mechanisms anticipate market action; if they are reacting to them, well that’s not exactly a mechanism discounting the future, is it?

This is a confusing time for investors; rather than repeat the clichés, let’s try to make some sense of all the cross-currents.

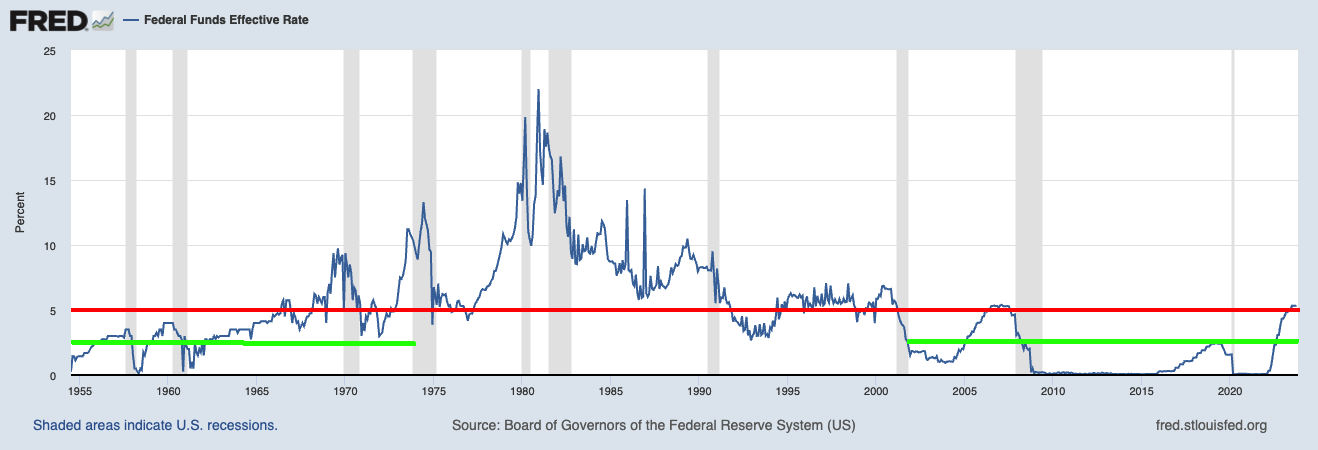

Federal Reserve: There is no such thing as a “Hawkish Pause.”

This is one of those phrases that really annoys me. It brings to mind Ralph Waldo Emerson’s insight: “What you do speaks so loudly I cannot hear what you are saying.”

The FOMC is either raising, not changing, or lowering rates, PERIOD. All of the chatter, speeches, transcripts, press releases, etc. are for those who prefer to spend their time sifting through the tea leaves for hints as to what’s coming next. My preference: look at what the Fed’s open market committee’s actions are.

To me, “Hawkish Pause” sounds a lot like a George Carlin bit on “Friendly Fire.”

Secular Bull Market: US stocks are in the 5-6th inning of a bull market.

The Pandemic crash and rally was a 34% reset and a continuation of the bull that formally began in March 2013.

BAML’s Chief Equity Technician Stephen Suttmeier likens the 2020 crash to the modern version of the 1987 crash: A substantial crash that took place 7 years into the start of a new bull. Historical comparisons imply this market may have another 3-7 years to go.

Cash in No Longer Trash: TINA (as we noted last year) is officially over.

525 basis points of hikes later, bonds are very attractive and fixed-income investors are earning a decent return on their money. If you are in a top tax bracket and have residency in a high-tax state with strong credit quality – think Ohio, New York, Massachusetts, California, Connecticut, etc. – you should be looking at Munis here. Depending on the specifics a 4.5-5% muni yield is the taxable equivalent of 8-10%.

Those of you looking for income might consider putting fresh money to work building a bespoke muni portfolio, or buying the appropriate muni fund for your circumstances. (we are happy to help).

Regime Change: The shift from monetary to fiscal stimulus.

The era of ultralow rates – that’s anything under 2% — has ended. While I expect to see rates moderate later in 2024 or 25, it’s a low probability bet they go back to zero.

The ramifications of this are significant: Bonds are now a competitor to equities; normalized rates might see this rally broaden out from Mega caps to Mid and Large Caps; the end of ZIRP could impact corporate profits; higher rates eventually will hurt consumer spending and CapEx. Note that these rates are normal for the post-war period but a bit high for the modern era.

~~~

Given all of the above, I would suggest you 1) maintain a diversified portfolio of equities; 2) lower your return expectations for those equities; 3) look to diversify globally as well; 4) revisit your bond portfolios; 5) consider Munis for tax free yield.

YMMV.

Previously:

Cash Is No Longer Trash (October 27, 2023)

Understanding Investing Regime Change (October 25, 2023)

Farewell, TINA (September 28, 2022)

Secular vs. Cyclical Markets (May 16, 2022)

End of the Secular Bull? Not So Fast (April 3, 2020)

Is the Secular Bear Market Coming to an End? (February 4, 2013)

Looking at the Very Very Long Term (November 6, 2003)