Michael Bloomberg: Building an Empire & Giving Away Billions

How did a layoff lead to a revolution in financial data? Mike Bloomberg shares the story behind the Bloomberg Terminal, lessons...

I’ve never shared this story before, but since we are at a milestone, I might as well… February 2000: I was working...

I’ve never shared this story before, but since we are at a milestone, I might as well… February 2000: I was working...

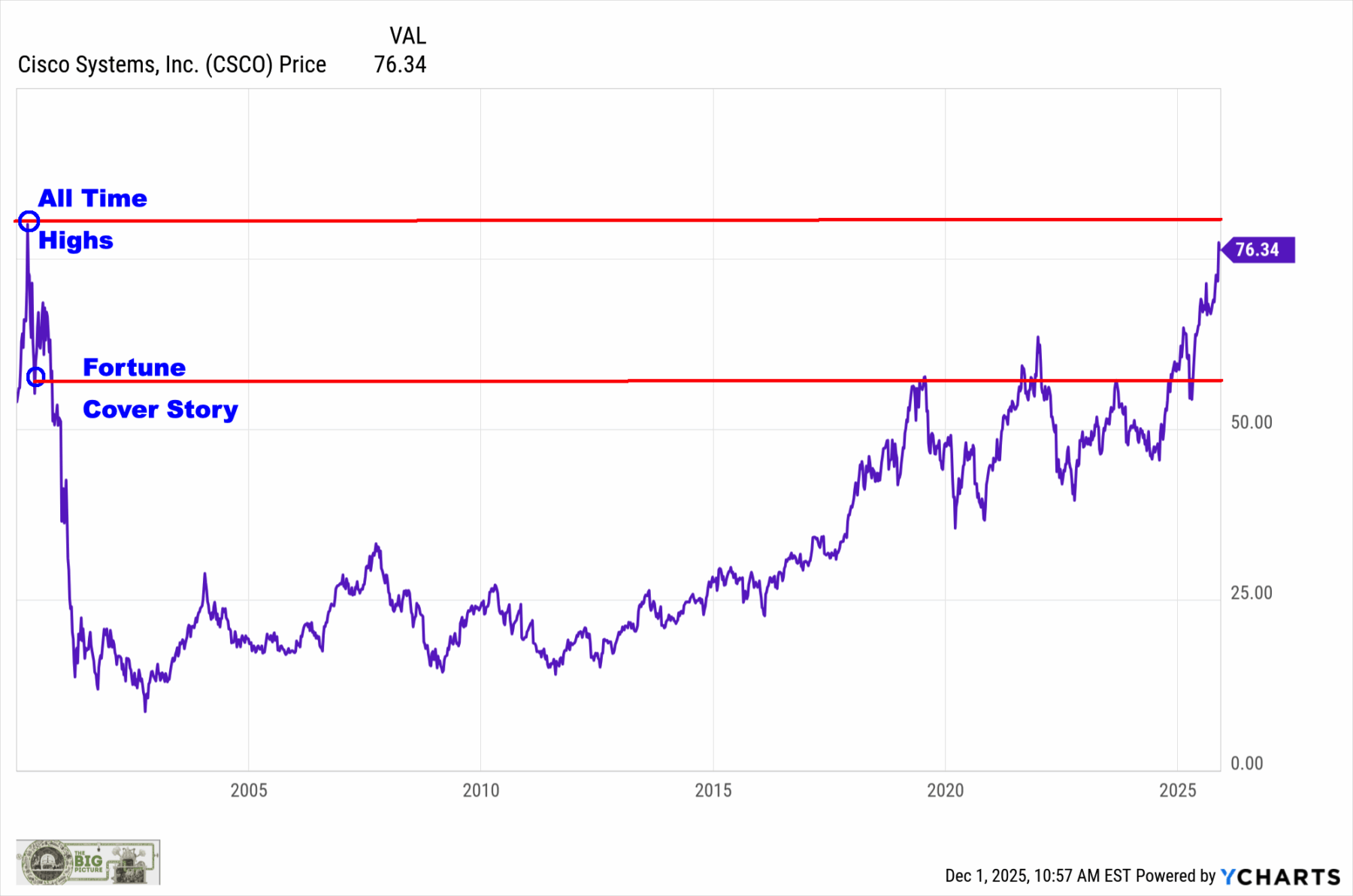

“Few outsiders think new stores, no matter how well-conceived, will get Apple back on the hot-growth path… Maybe...

“Few outsiders think new stores, no matter how well-conceived, will get Apple back on the hot-growth path… Maybe...

First, the data (via Bloomberg): 5,502,284% That is the per-share market value increase of Berkshire Hathaway stock from 1964...

First, the data (via Bloomberg): 5,502,284% That is the per-share market value increase of Berkshire Hathaway stock from 1964...