Transcript: Erika Ayers Badan, Barstool Sports

The transcript from this week’s, MiB: Erika Ayers Badan, CEO of Barstool Sports, is below. You can stream and download...

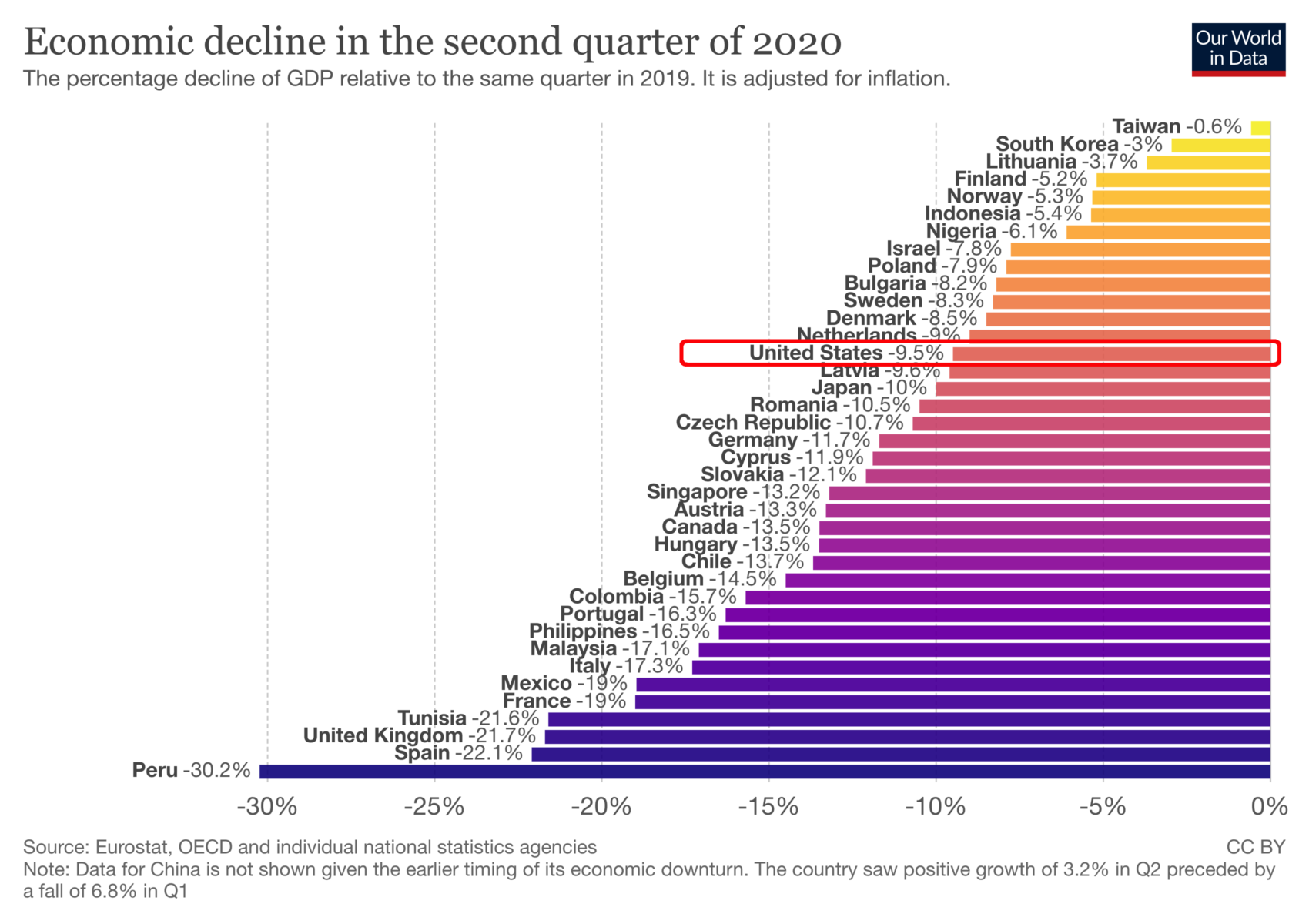

Source: ourworldindata Every Tuesday for the past 7 years, I get an email. It is a reminder I send to myself via...

Source: ourworldindata Every Tuesday for the past 7 years, I get an email. It is a reminder I send to myself via...

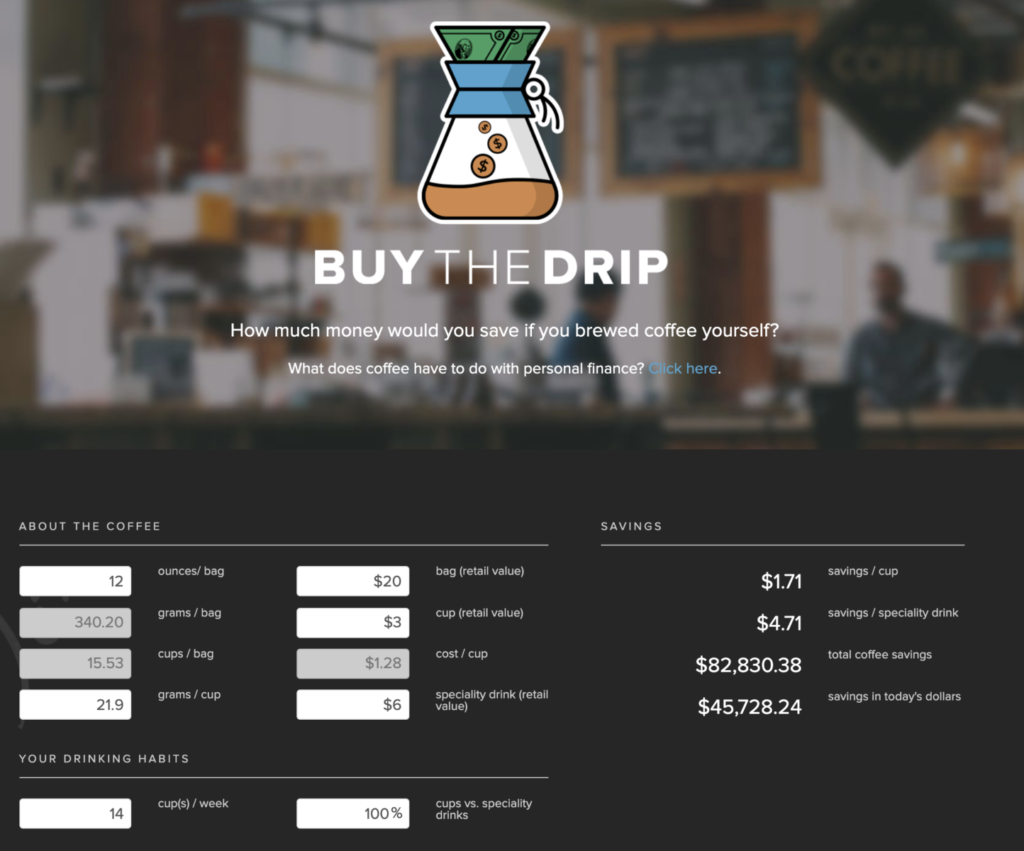

Its a Summer Friday — a perfect time for something I have been meaning to get to posting on: Buy the Drip! (Kashana Cauley post...

Its a Summer Friday — a perfect time for something I have been meaning to get to posting on: Buy the Drip! (Kashana Cauley post...

Get subscriber-only insights and news delivered by Barry every two weeks.