A conversation with Jim Simons

During the 2022 Abel lectures Jim Simons had a conversation with Nils A. Baas and Nicolai Tangen. The lectures were held at The...

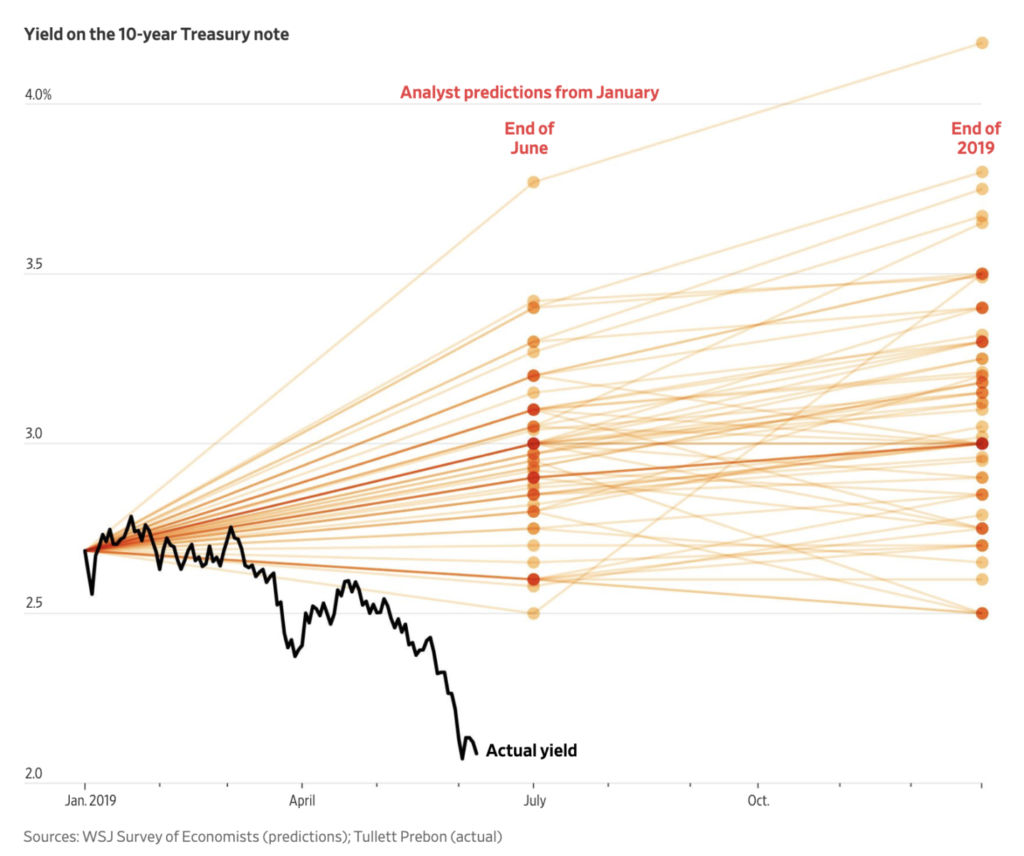

Source: WSJ From the really, really bad calls file: Last week, I showed this great chart by Torsten Sløk of Deutsche Bank. It...

Source: WSJ From the really, really bad calls file: Last week, I showed this great chart by Torsten Sløk of Deutsche Bank. It...

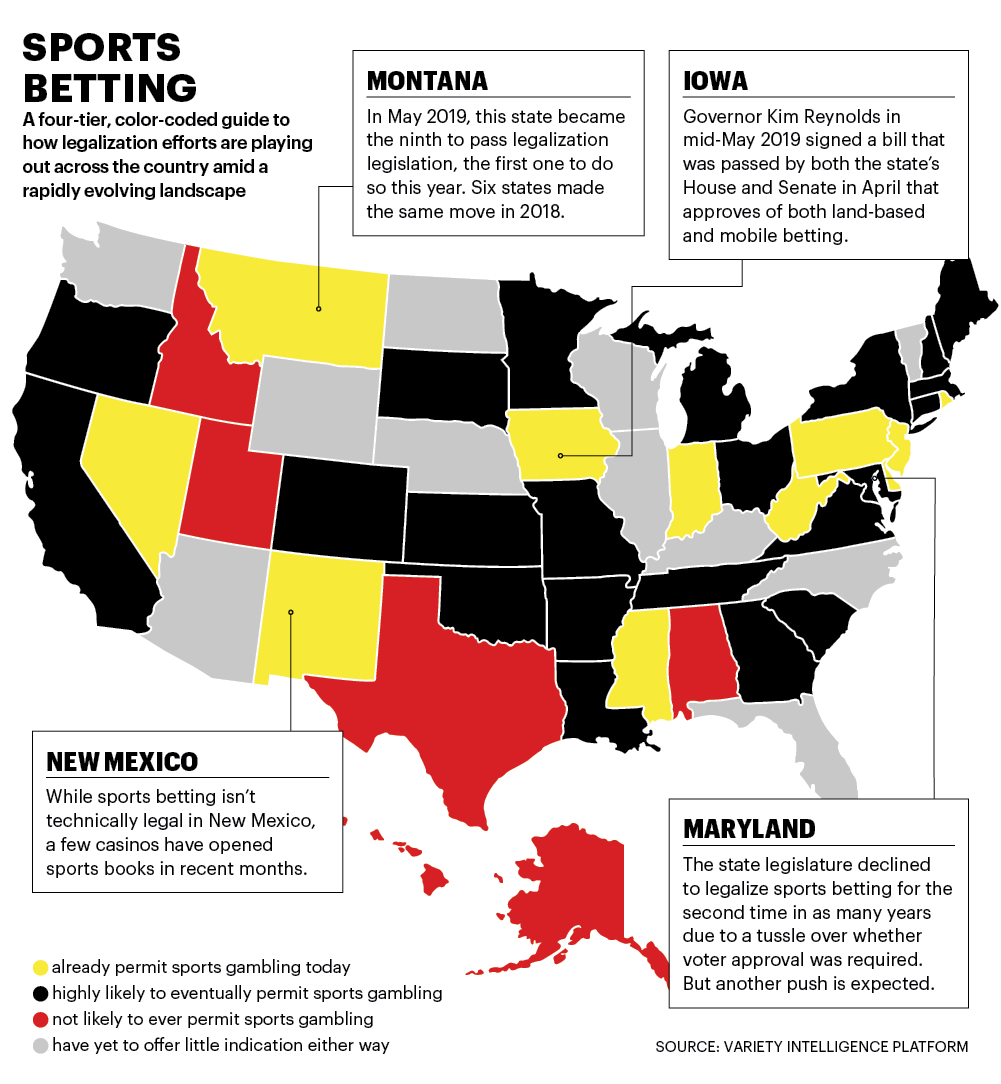

Sports betting is now legal in 11 states (including Nevada). Source: Variety Its been a year since the U.S. Supreme Court struck...

Sports betting is now legal in 11 states (including Nevada). Source: Variety Its been a year since the U.S. Supreme Court struck...

Get subscriber-only insights and news delivered by Barry every two weeks.