Why You Should Stick With `Buy and Hold’ Beware of those who claim they have a strategy to capture the upside of market volatility and...

Read More

In Defense of Wall Street Jack Bogle, the Vanguard founder, has it wrong: The financial-services industry does add value to the economy....

Read More

Why You Should Stick With `Buy and Hold’ Beware of those who claim they have a strategy to capture the upside of market volatility and...

Read More

Whenever a company offers something at no charge, that means the price is hidden and out of sight. Investors considering the plethora of...

Read More

Translation of an article by Hyun Song Shin, Economic Adviser and Head of Research of the BIS, in the Frankfurter Allgemeine...

Translation of an article by Hyun Song Shin, Economic Adviser and Head of Research of the BIS, in the Frankfurter Allgemeine...

Read More

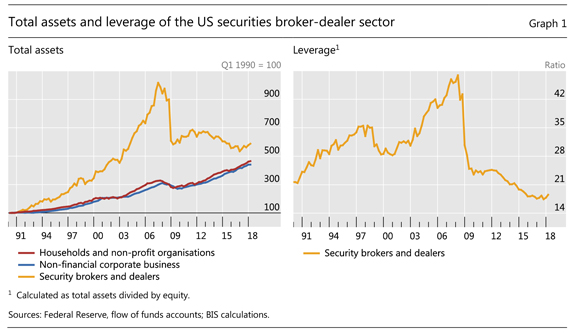

The 10 year anniversary of the financial crisis is here next month — the remembrances will be coming fast and furiously. This...

The 10 year anniversary of the financial crisis is here next month — the remembrances will be coming fast and furiously. This...

Read More

This week, on our Masters in Business radio podcast, we speak with Richard Sylla, professor emeritus of economics at New York...

Read More

How to Avoid Going Broke After Making $650 Million Even a large fortune can be squandered in a short time. Bloomberg, June 29, 2018...

Read More

Ten Reasons Finance Will Keep Changing Constant flux is the norm. Get used to it. Bloomberg, June 22, 2018 One of...

Read More

Ten Reasons Finance Will Keep Changing Constant flux is the norm. Get used to it. Bloomberg, June 22, 2018 I spoke at the...

Read More