Making good progress on the book, about 60-70% finished (I feel good about it). I wanted to pop out of hiding to share a...

Making good progress on the book, about 60-70% finished (I feel good about it). I wanted to pop out of hiding to share a...

Read More

The transcript from this week’s, MiB: Jeffrey Sherman, DoubleLine Deputy CIO, is below. You can stream and download our...

Read More

This week, we speak with Jeffrey Sherman, deputy chief investment officer at DoubleLine Capital. Sherman oversees and...

Read More

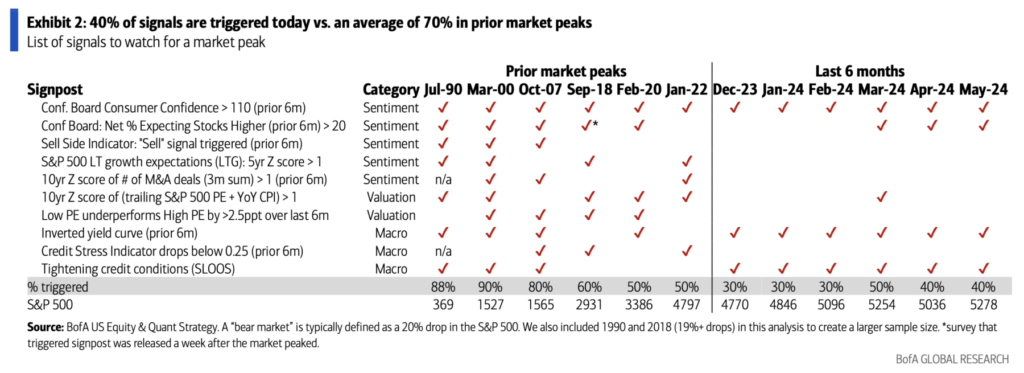

The transcript from this week’s, MiB: Savita Subramanian, US Equity & Quantitative Strategy, Bank of America, is...

Read More

This week, we speak with Savita Subramanian, head of US Equity and Quantitative strategy at Bank of America. She also leads...

Read More

At the Money: Benefits of Quantitative Investing (March 20, 2024) Throughout history, investing has been a lot more...

Read More

The transcript from this week’s, MiB: Linda Gibson, CEO, PGIM Quantitative Solutions, is below. You can stream and...

Read More

This week, we speak with Linda Gibson, who is CEO of PGIM‘s Quantitative Solutions, a pioneer in quant investing...

Read More

The transcript from this week’s, MiB: Jon McAuliffe, the Voleon Group, is below. You can stream and download our...

Read More

This week, we speak with Jon McAuliffe, who is co-founder and chief investment officer at the Voleon Group, heading the...

Read More