The following speech was delivered by Ray Dalio of Bridgewater at the Federal Reserve Bank of New York’s 40th Annual Central Banking Seminar on Wednesday, October 5, 2016.

~~~

It is both an honor and a very special opportunity for me to be able to address such a large and esteemed group of central bankers at such an interesting time for central bankers. I especially want to thank President Dudley and Vice President Schetzel for inviting me to forthrightly share my perspective as an investor and my unconventional template that I believe sheds some light on the very unconventional circumstances that we face.

It is no longer controversial to say that:

• …this isn’t a normal business cycle and we are likely in an environment of abnormally slow growth

• …the current tools of monetary policy will be a lot less effective going forward

• …the risks are asymmetric to the downside

• …investment returns will be very low going forward, and

• …the impatience with economic stagnation, especially among middle and lower income earners, is leading to dangerous populism and nationalism.

While these things are now widely agreed, there still isn’t agreement on why these things are true or what to do about them. While there are many factors at play, I believe that the most important ones are covered by a simple template that I use to guide my global macro investing.

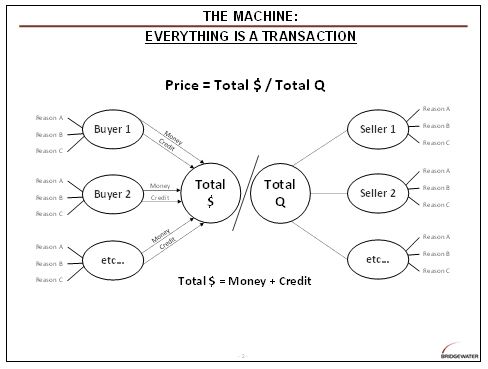

To me an economy is nothing more than the aggregate of the markets that make it up, and that to understand what is going on, we need to look at who is doing what buying and selling of goods, services and financial assets, and why. That understanding is essential for us to understand market prices and volumes. We try to put ourselves in the shoes of the major buyers and sellers to understand what they are doing and why, and then project what they will do. By looking at the major buyers to estimate how much money and credit they will spend and the major sellers to estimate what quantities they will sell, we divide the total amount spent by the total quantity to determine the price.

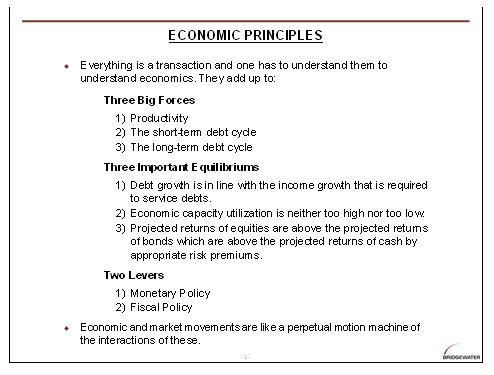

From watching these transactions from both the micro level up and the macro level down, we see them add up to three main forces that all drive all economies:

1) Productivity growth

2) The short-term debt cycle, also known as the business cycle, which typically takes 5 to 10 years, and

3) The long-term debt cycle, which typically takes 50 to 75 years.

I believe that the most important force that is now driving what is happening and isn’t well understood is the long-term debt cycle. Long-term debt cycles are not well understood because they come along only once in a lifetime.

There are also three important equilibriums that economies and markets gravitate towards:

1) Debt growth has to be in line with the income growth that services those debts

2) Economic operating rates and inflation rates can’t be too high or too low for long, because if an economy is depressed or too hot for long, that will lead to changes to reverse it, and

3) The projected returns of equities have to be above the projected returns of bonds which have to be above the projected returns of cash by appropriate risk premiums.

The most important differences that will exist in the future that did not exist in the past are that debt will not be able to rise as fast and the capital markets transmission mechanism won’t work as well, as interest rates can’t be lowered and risk premiums of other investments are low and shrinking. If appropriate risk premiums don’t exist, the transmission mechanism of capital won’t work as well and the economy will grind to a halt. For these reasons major central banks are facing a “pushing on a string” situation. The last time this happened was in the late 1930s.

There are two levers that policy makers use to bring about these equilibriums:

1) Monetary policy, which operates via interest rate changes and “quantitative easings”, which depend on significant central bank purchases and appropriate capital market risk premiums, and

2) Fiscal policy, which depends on political coordination both within the central government and with the central bank’s monetary policy.

Economic and market movements are like a perpetual motion machine of interactions of these. The most profound differences that now exist are the relative impotence of monetary policy and political fragmentation that makes coordination of fiscal and monetary policies hard to imagine.

Where does that leave us now?

By and large:

1) Productivity growth is slow, though properly accounting for it has never been more difficult

2) The short-term debt/business cycles as measured by GDP gaps are closer to their mid-points than to their extremes, and

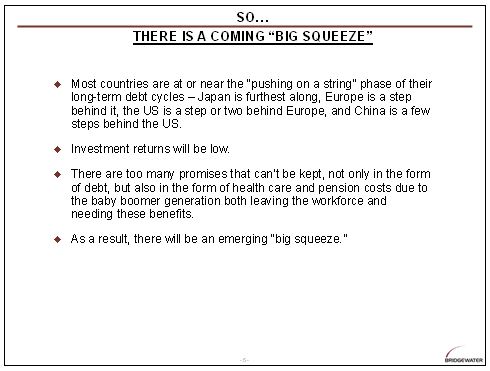

3) The long-term debt cycles are approaching their very late-stages as debts can’t be raised much and central banks are approaching “pushing on a string” limitations to their effectiveness.

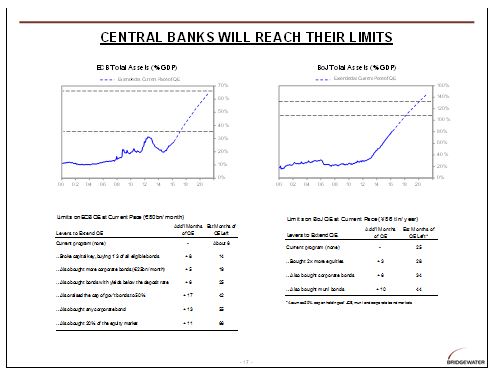

The biggest issue is that there is only so much one can squeeze out of a debt cycle and most countries are approaching those limits. In other words, they are simultaneously approaching both their debt limits and central banks’ “pushing on a string” limits. Central banks are approaching their “pushing on a string” limits both because interest rates are approaching their maximum lows, and because the effectiveness of QE is approaching its limits as the risk premiums and spreads are compressing. Also, the wealth gap and numerous other factors make lending to spenders more challenging. This is a global problem. Japan is closest to its limits, Europe is a step behind it, the US is a step or two behind Europe, and China is a few steps behind the United States.

Unlike in 2007 when this template signaled that we were in a bubble and a debt crisis lay ahead, I don’t see such an abrupt crisis in the immediate future because a) most economies are near the mid-points of the short-term debt cycles and their growth rates are neither dangerously rapid nor dangerously slow – i.e. the cyclical influences are close to being in equilibrium – and b) debt growth rates in the developed countries have been roughly in line with income growth rates with debts largely in the hands of central bankers who can roll them forward.

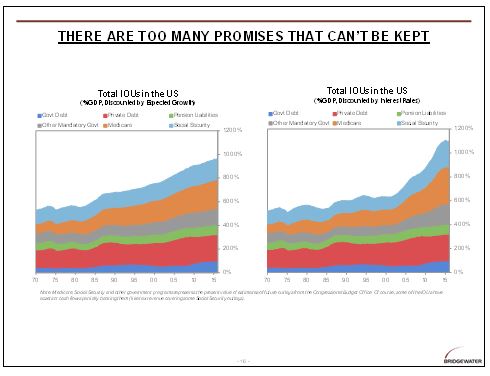

However, when we do our projections we see an intensifying financing squeeze emerging from a combination of slow income growth, low investment returns and an acceleration in liabilities coming due both because of the relatively high levels of debt and because of large pension and health care liabilities. The pension and health care liabilities that are coming due are much larger than the debt liabilities in most countries because of demographics – i.e., due to the baby-boom generation moving from working and paying taxes to getting their retirement and health care benefits.

I think of the gap between projected liabilities and projected incomes in the following way. Holders of debt believe that they are holding an asset that they can sell for money to use to buy things, so they believe that they will have that spending power without having to work. Similarly, retirees expect that they will get the retirement and health care benefits that they were promised without working. So, all of these people expect to get a huge amount of spending power without producing anything. At the same time, workers expect to get spending power that is equal in value to what they are giving. They all can’t be satisfied.

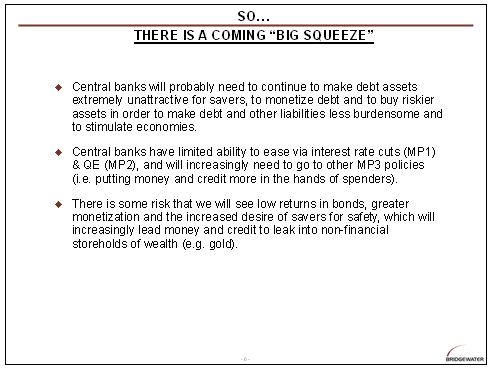

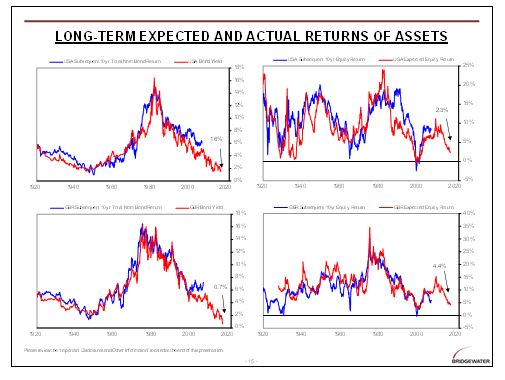

As a result of this confluence of conditions, we are now seeing most central bankers pushing interest rates down to make them extremely unattractive for savers and we are seeing them monetizing debt and buying riskier assets to make debt and other liabilities less burdensome and to stimulate their economies. Rarely do we investors get a market that we know is over-valued and that approaches such clearly defined limits as the bond market now. That is because there is a limit as to how negative bond yields can go. Their expected returns relative to their risks are especially bad. If interest rates rise just a little bit more than is discounted in the curve it will have a big negative effect on bonds and all asset prices, as they are all very sensitive to the discount rate used to calculate the present value of their future cash flows. That is because with interest rates having declined, the effective durations of all assets have lengthened, so they are more price-sensitive. For example, it would only take a 100 basis point rise in Treasury bond yields to trigger the worst price decline in bonds since the 1981 bond market crash. And since those interest rates are embedded in the pricing of all investment assets, that would send them all much lower.

At the same time, as bonds become a very bad deal and central banks try to push more money into the market and yields go even lower and price risks increase further, savers might decide to go elsewhere. At existing rates of central bank buying—which I believe will be required for the foreseeable future—central banks are going to start to hit the limits of their existing constraints. Those limits were put into place because they originally thought that they were prudent but they are going to have to go buy other things. Right now, a number of the riskier assets look attractive in relationship to bonds and cash, but not cheap in relationship to their risks. If this continues, holding non-financial storeholds of wealth like gold could become more attractive than holding long duration fiat currency flows with negative yields (which is what bonds are), especially if currency volatility picks up.

Concerning what policies will likely be required of central bankers given the reduced effectiveness of interest rate cuts and quantitative easing, and assuming that political limitations on fiscal policies and structural reforms remain stringent, it appears to me that there will have to be greater purchases of riskier assets and more direct placements of purchasing power in the hands of spenders, especially as the previously described squeeze intensifies.

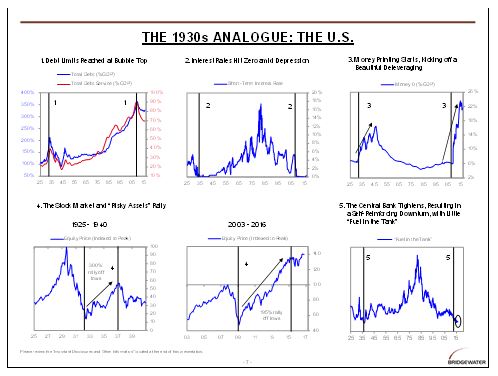

While no period is entirely analogous, the most recent similar period for the world economy as a whole was 1935-45. After the debt-financed bubble of the late 1920s (which was analogous to the debt financed bubbles of the 2005-07 period), and after the 1929-32 stock market and economic dives (like those in 2008), and following the great quantitative easings that caused stock prices and economic activity to rebound (like those we saw since 2008), came “pushing on a string” in 1935, for analogous reasons – i.e. interest rates and risk premiums approached 0%.

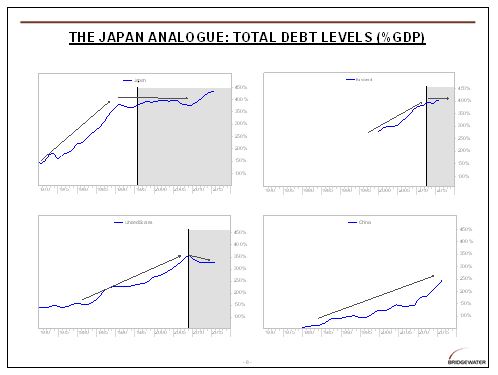

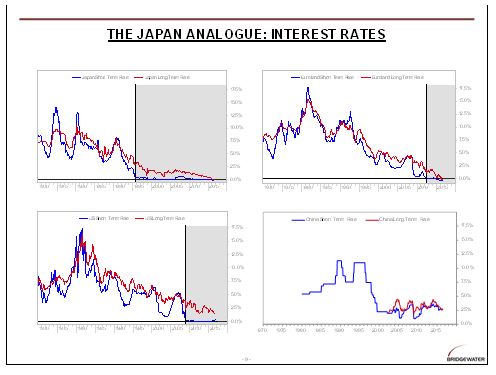

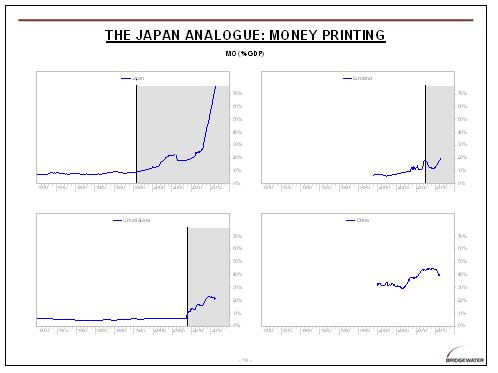

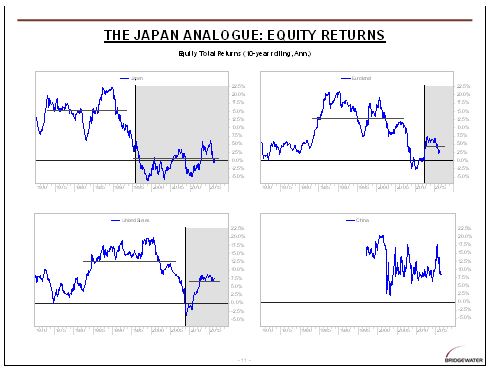

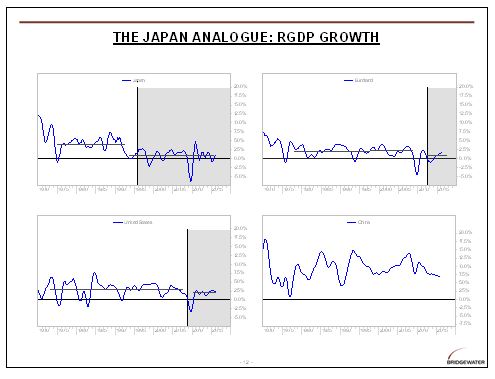

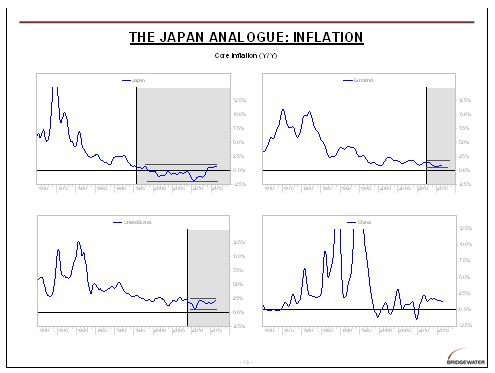

Similarly, the last 20 years in Japan are analogous in that there has been a similar combination of high levels of indebtedness, interest rates hitting 0%, risk premiums and asset returns shrinking, growth and inflation being low, and “pushing on a string” being a problem.

Appendix:

Source: LinkedIn

Important Disclosures and Other Information

Bridgewater research utilizes data and information from public, private and internal sources, including data from actual Bridgewater trades. Sources include, the Australian Bureau of Statistics, Asset International, Inc., Barclays Capital Inc., Bloomberg Finance L.P., Capital IQ, Inc., CEIC Data Company Ltd., Consensus Economics Inc., Credit Market Analysis Ltd., CreditSights, Inc., Crimson Hexagon, Inc., Corelogic, Inc., Dealogic LLC, Ecoanalitica, Emerging Portfolio Fund Research, Inc., Factset Research Systems, Inc., The Financial Times Limited, Fundata Canada, Inc., GaveKal Research Ltd., Global Financial Data, Inc., Haver Analytics, Inc., Intercontinental Exchange (ICE), Investment Company Institute, International Energy Agency, Investment Management Association, Markit Economics Limited, Mergent, Inc., Metals Focus Ltd, Moody’s Analytics, Inc., MSCI, Inc., National Bureau of Economic Research, Organisation for Economic Co- operation and Development, Paramita Tecnologia Consultoria Financeira LTDA, Property and Portfolio Research, Inc., RealtyTrac, Inc., RP Data Ltd, Rystad Energy, Inc., Sentix Gmbh, Shanghai Wind Information Co., Ltd., Spears & Associates, Inc., Standard & Poor’s Financial Services LLC, State Street Bank and Trust, Thomson Reuters, Tokyo Stock Exchange, TrimTabs Investment Research, Inc., United Nations, US Department of Commerce, World Bureau of Metal Statistics, World Economic Forum, and Wood Mackenzie Limited. While we consider information from external sources to be reliable, we do not assume responsibility for its accuracy.

The views expressed herein are solely those of Bridgewater and are subject to change without notice. In some circumstances Bridgewater submits performance information to indices, such as Dow Jones Credit Suisse Hedge Fund index, which may be included in this material. You should assume that Bridgewater has a significant financial interest in one or more of the positions and/or securities or derivatives discussed. Bridgewater’s employees may have long or short positions in and buy or sell securities or derivatives referred to in this material. Those responsible for preparing this material receive compensation based upon various factors, including, among other things, the quality of their work and firm revenues.

This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. Any such offering will be made pursuant to a definitive offering memorandum. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment or other advice. The information provided herein is not intended to provide a sufficient basis on which to make an investment decision.

No part of this material may be (i) copied, photocopied or duplicated in any form by any means or (ii) redistributed without the prior written consent of Bridgewater Associates ®, LP.

©2016 Bridgewater Associates, LP. All rights reserved.

What's been said:

Discussions found on the web: