Source: JP Morgan

To hear an audio spoken word version of this post, click here.

I have been saving this table and chart since Michael Cembalest of JP Morgan published it in November 2020. Since it’s that time of year, I thought it was worth reminding you a few things about punditry and year-end forecasts and all the rest of the usual unhelpful noise out there.

1. Agenda: Everyone has their own agenda. Whether it’s selling their consulting services or ETFs or IPOs or clicking on their advertising, there is always something a pundit wants out of you.

Me too: I have a wealth management firm, so I want your portfolio; I host a podcast, so I want you to listen; I write books and columns and blogs so I want your attention to read them. But not everyone’s agenda is clearly disclosed. Be aware of what people may want from you when they are arguing pro or con for any specific investment idea.

2. Your Goals: You should be thinking for yourself and not imitating either extreme: the ministers without portfolios or billionaires or others whose financial needs are very different than yours. Billionaires are protecting their wealth and leaving a legacy; your needs are likely very different than theirs.1 Recognize this and adjust accordingly.

3. Beware the Narratives: One of the oddest aspects of this is the changing storylines around various talking heads. My favorite piece about this is Josh’s discussion of Joe Granville. The modern version has been the intense media scrutiny on Cathie Wood of ARK. In 2020, the narrative was Wood as a seer, someone who could do no wrong; 2021 revealed a new narrative: She just got lucky the prior year.

As always The Truth is far more nuanced and complicated than either of those claims. Wood runs a concentrated high-octane portfolio of innovative tech companies that are very volatile. When they are in favor, they have wildly outperformed; when they are out of favor, they badly lagged. That nuance is a much less interesting media story than 1) her “Amazing Crystal Ball” 2) that “Suddenly was Broken.”

4. Fashion: Pundits come into and out of fashion like, well fashion. Hemlines rise and fall, colors come in and go out of favor, styles change. The clothing industry changes fashion to drive consumers to make new purchases to refresh their wardrobes. The media sees the rise and fall of specific Pundits for the same reason: There is always a need for fresh meat to feed the daily beast.

5. Bylines over Mastheads: I have found it to be enormously helpful to build a stable of people I can rely on. They have a long-term track record of “providing light” instead of heat; they raise interesting ideas in intelligent ways and force me to think in ways I may not have otherwise. My list of these folks is pretty long, but you can find most of the people whose insights I most rely upon and value either on MiB or working with me at RWM.

You should create your own list — not just of people with whom you agree, but whose track records and ability to communicate truly add value. They should inform and provoke you, make you rethink your own assumptions. If they can make you clarify your own thoughts, and sharpen your arguments, they are potentially worth including in your list.

~~~

On Monday I mentioned this is the “Most Forecasty Time of the Year,” but really, this is a year-round concern. Whether you are bullish or bearish, there is a pundit out there just waiting to satisfy your confirmation bias. Instead, find a better way to let smart, insightful people inform your worldview, while still retaining your own independence of thought.

Previously:

The Unofficial Pundit to English Translation Guide (June 29, 2016)

The Halo Effect: Bad Forecasts by Billionaires (December 18, 2015)

Why Don’t We Hold Pundits Accountable? (June 11, 2014)

Pundit Suckitude: Its a feature, not a bug. (July 30, 2013)

The PermaBear to English Translation Guide (October 15, 2010)

Forecasting & Prediction Discussions

________

1. My favorite example was a 2006 article touting Michael Dell’s purchase of $70M worth of Dell stock. It was his first-ever purchase of his namesake company’s stock — he had been steadily selling every year since 1988, which is how he amassed a $19B fortune. It was roughly the equivalent of an average investor buying 100 shares of Dell — for more, see Dell Makes A Purchase (Whoopee!).

click for audio

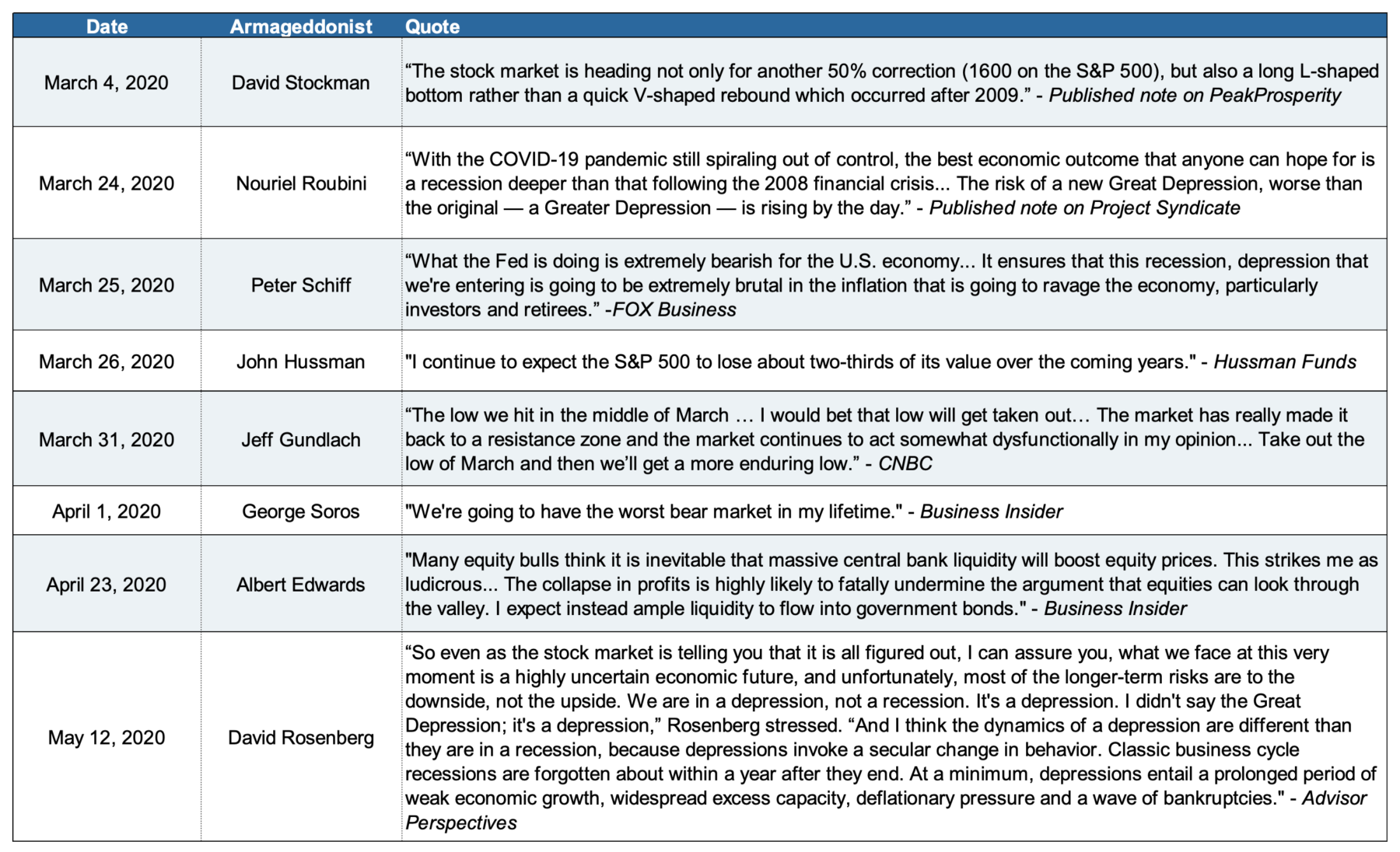

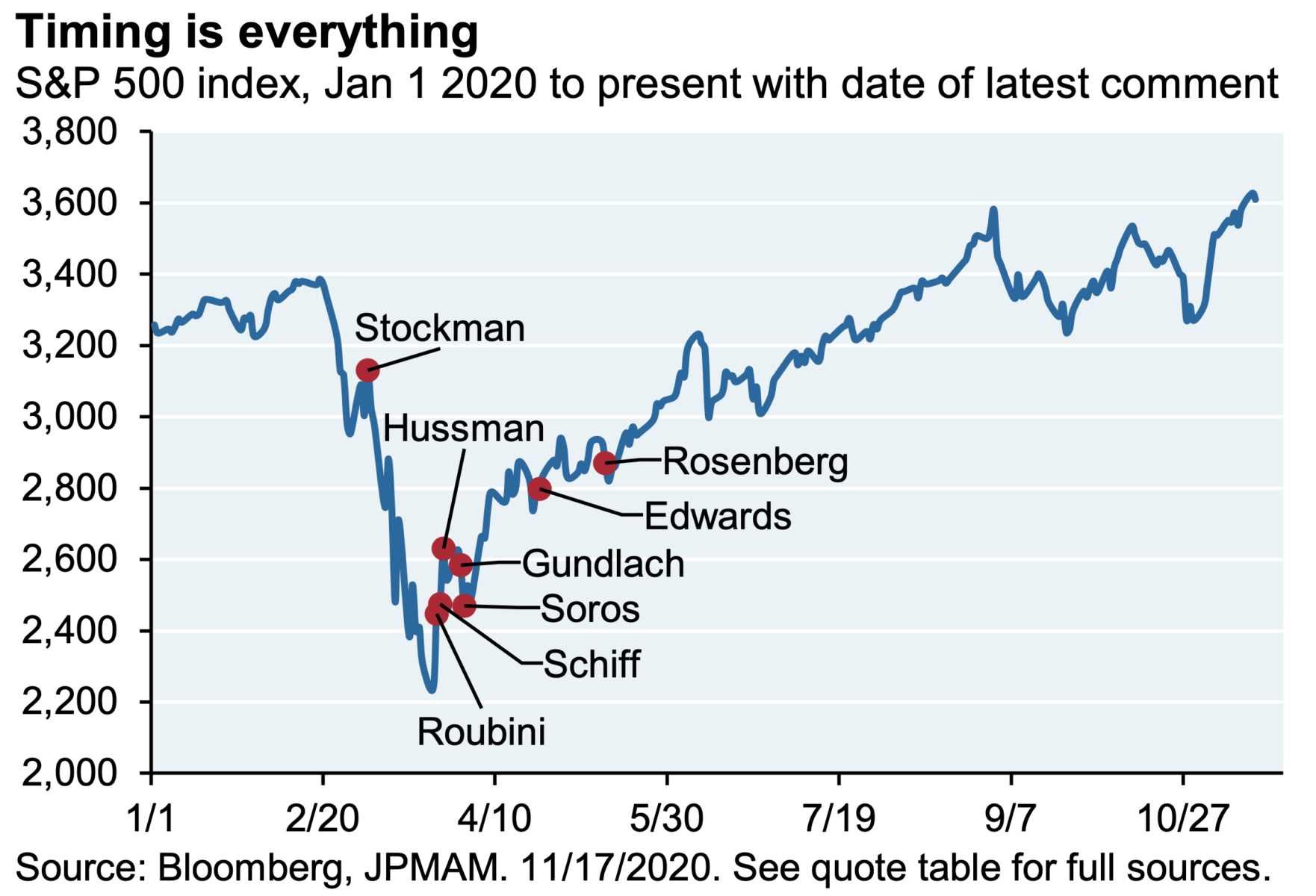

The Armageddonists

Source: JP Morgan