I keep hearing comments and concerns about these markets in the media. Since my wife is tired of me yelling at the television (“No! That’s wrong!”) you are the lucky recipients of my ire.

Here are five things I have been thinking about regarding markets, the economy, and investments – from the most bullish to the least – that are too easily misunderstood:

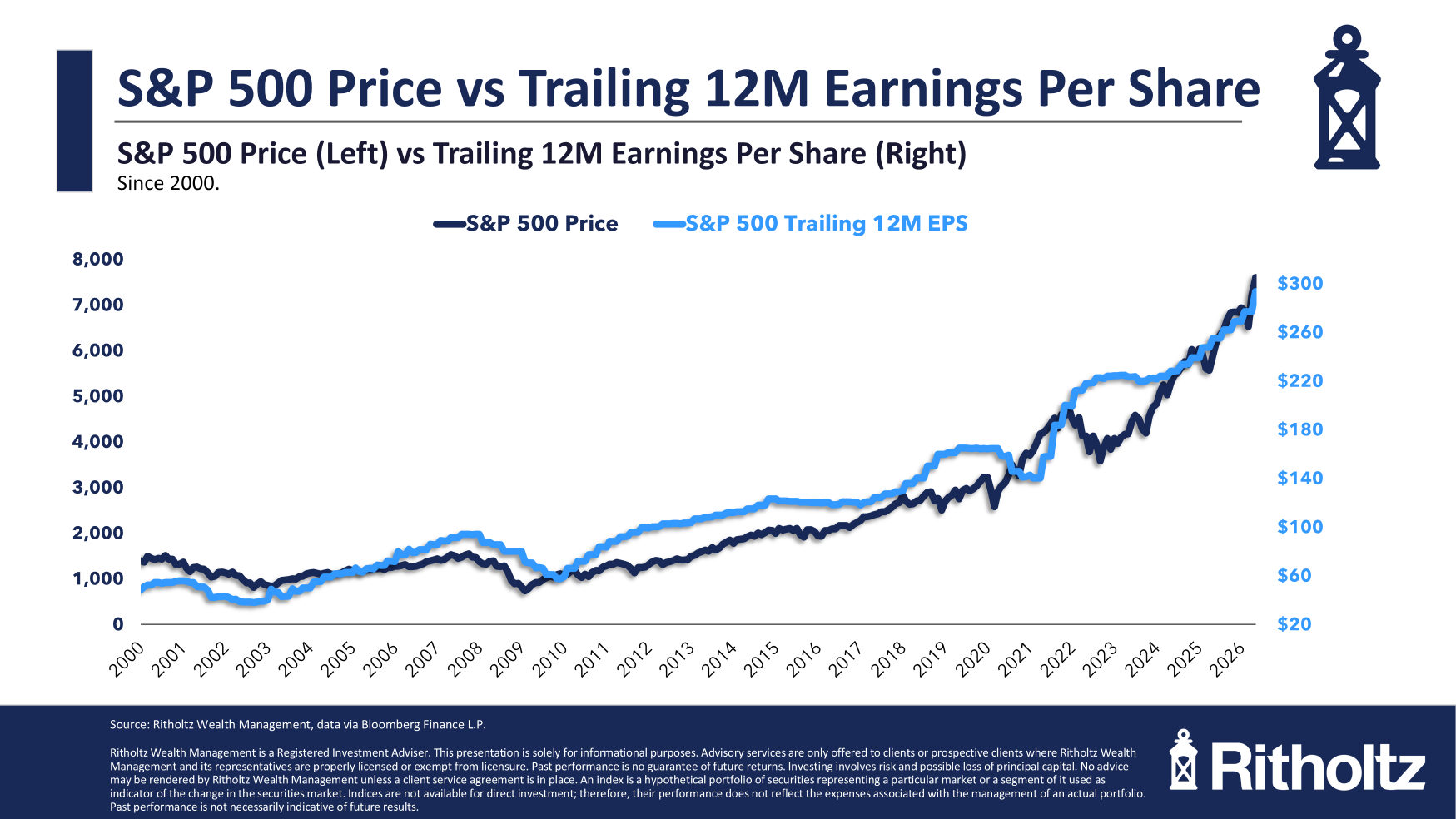

1) Profits: If I can only look at one data point to gauge the overall direction of equity markets, it would be profits. And, corporate profits have been on a tear the past few years.

To be sure, the hyperscalers’ artificial intelligence buildout and massive CapEx are significant factors. But we have also seen good profits in sectors ranging from Communication Services, Health Care, Financials, Consumer Discretionary, and Materials — all are having strong quarters; (unsurprisingly, Consumer Discretionary is the least consistent).

And these are not just one-time blips; we have enjoyed the rare combination of record profits and record profit growth rates. If you want to understand what has been driving equity prices, look no further than this powerful one-two punch.

At the same time, high(ish) valuations have become a little cheaper, as multiples have compressed. This is very powerful…

2) All-Time Highs: The data is unequivocal. Investing at all-time highs yields better returns than at all other dates. I have been saying this for years, so rather than repeat myself, I will let Sam Ro give you the details:

“Just because major market drawdowns are often preceded by record highs doesn’t mean all-time highs are often followed by major market drawdowns. Hopefully, this is obvious. The stock market would not have trended higher for decades if this were not true. Eyeball any long-term chart of the stock market, and you’ll see all-time highs followed by new all-time highs.”

There were over 493 new all-time highs from 1983 to 2000. Except for the very last one, every single one of these was bullish.

If you want to make a bet against 500 to 1 odds, well, that’s your call. I am on the other side of that trade.

3) Sentiment: Another intriguing issue that keeps coming up is record lows in U Mich Sentiment. Many find this deeply concerning.

But here is the thing: Your individual sentiment is based on what you experience personally – in BeFi terms, the “Availability Heuristic” of what is in your personal economy. But that is not what drives markets. We discussed this in terms of the pandemic and, more recently, how we can have all-time highs in equities with all-time lows in consumer sentiment.

Most of the time, Sentiment measures do not provide a very clear signal. The contrarian in me looks at record low sentiment measures as a potentially bullish indicator…

4) K-Shaped Economy: Here is the disappointing, grim reality: Throughout most of human history, it has been a very “Winner takes all (or most)” kind of economic system.

The challenge is in having the top 10% of the economic strata driving half of the economic activity. This may not be a sustainable situation — economically or politically.

There were hopes that the industrial revolution, unionization, and the general rise in entrepreneurship might push back against that reality. But it is looking more and more like the Roaring 1920s, the 1980s bull market, the post-GFC bailouts were the norm, not the exception.

I grew up in the post-war era, and I took it for granted that it was the norm. I am starting to suspect exactly how aberrational that period was. It is looking more and more like the entire post-war period – the rise of the middle class, the build-out in the USA of suburbia, interstate highways, the electronics industry, semiconductors, manufacturing, civilian aviation, etc. – was a historical aberration.

I hope this is incorrect, but fear it is not…

Iran War / Oil / Inflation: Venezuela was fast and easy; Cuba is likely a bit more difficult. But Iran has its own strategic, tactical, and military assets; it is its own player in the Middle East. Oh, and they have been supplying drones to Russia (!) for its war against Ukraine.

I have no idea how the Dunning-Kruger War will ultimately play out in terms of energy prices and/or inflation, but it appears not to have been well thought out in advance.

The good news is regional wars generally don’t impact stock prices much; the bad news is this is the one with the potential for causing exactly that kind of mischief…

~~~

Generally speaking, I am bullish on US equities and even more bullish on overseas bourses. There are signs of froth and foolishness, none of which rise to systematic problems.

Am I happy about the excesses surrounding the SpaceX IPO? Absolutely not. The index gaming from Nasdaq and S&P is deeply problematic and disappointing. But it does not read to me as a market killer.

If you have learned anything from this market over the past 15 years, it is that it deserves the benefit of the doubt. The economy has been cooling, but not outright decelerating. Housing is a mess, still working off the excesses of the GFC. College grads seem to be having a hard time finding jobs.

It’s not perfect out there. But until we see deeper signs of deterioration and further economic weakening, I remain constructive…

Previously:

All Time Highs (SP500) versus All Time Lows (Consumer Sentiment) (April 24, 2026)

Maybe Mr. Market Is Rational After All… (August 7, 2020)

The K-Shaped Recovery (September 4, 2020)

No, Market Highs Are Not a Bad Sign (March 5, 2014)

The Bifurcated Recovery in Jobs (November 12, 2013)