There’s nothing like confusing market action to send people into narrative creation overdrive. Yesterday’s 2% collapse on hotter-than-expected CPI data, followed by ~5% recovery to finish the day up more than 2% is a perfect example of random market action begetting endless explanations.

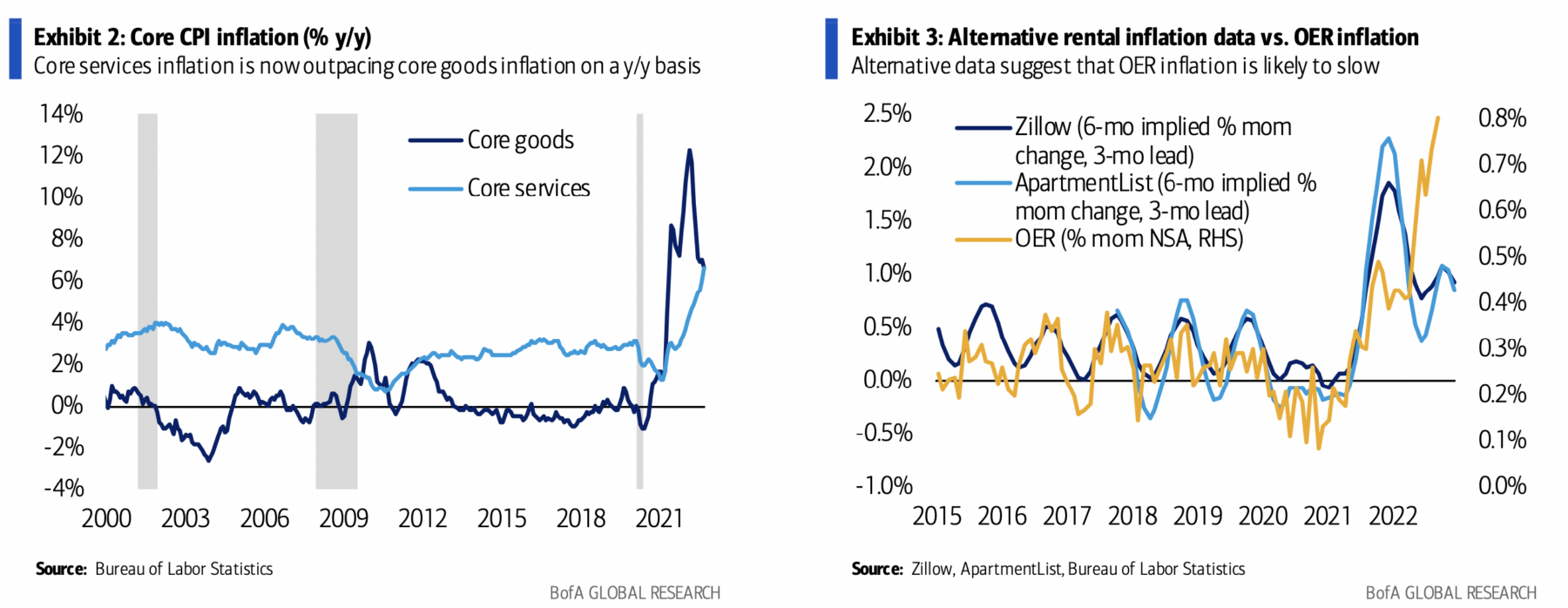

What was the takeaway from CPI? Check out the BAML chart above: Core goods are coming down (that’s good!), but core services are still rising (that’s bad!). Rent is nearly half of CPI (and most of the services portion), so consider alternative measures of rent — they show it’s not as hot as officially reported (which is good!) unless the Fed ignores it (which is bad?).

Perhaps this explains why the data was so confusing; no wonder we had so many after-the-fact explanations:

-Markets had given back 50% of the post Covid rally, a key technical support;

-The strong dollar is making imports much cheaper;

-Owners equivalency rent (OER) is creating a misleading gauge of services inflation;

-The Fed is showing signs of pivoting;

-Program trading kicked in at the lows;

-The residential real estate collapse is occurring faster than expected;

-It’s all already priced into the market.

I don’t want to suggest any of these explanations are inaccurate — they could all be correct! But rather, I want to point out that they were as true before yesterday’s reversal as they were after. The issue is of causation, not understanding.

The simple truth is that Humans prefer narrative descriptions of what just happened regardless of accuracy; certainly, we are more comfortable with these than we are with accepting that the universe is random. “Sometimes, markets be batshit crazy!” is not an explanation that anybody loves . . .

Where does that leave investors today?

Some market bottoms are a process, a blind groping of various market participants with different risk tolerances, financial goals, and time horizons.

Capitulation is a term used to describe the sorts of lows we see when secular bear markets end: the overwhelming powerful sale of everything. However, the more cyclical bear markets tend to make lows that occur over time as sentiment shifts and new info works its way into the psychology of traders. I think more of a range and less of a point than the full-on capitulatory surrenders of the secular, generational lows.

I mentioned at the end of September we were in the 7th Inning Stretch; where does that leave us today?

The risk here feels asymmetric: The downside appears to me as a potential grind lower — the Fed overtightens, then keeps over-tightening; maybe earnings miss badly; That mild recession we have been discussing — what if it turns out to be much worse than expected?

But the upside feels potentially explosive: One mild CPI print (imagine year-over-year with a 6-, or heaven forbid, a 5-handle!) or a really bad NFP report; what happens to the price of Oil when Russia pulls out of Ukraine?

This is inexact, more art than science.

See also:

Bad News is Good News (Batnick, October 14, 2022)

September consumer inflation: a function of the fictitious “Owners’ Equivalent Rent” + new cars: (Bond Dad, October 13, 2022)

Previously:

7th Inning Stretch (September 30, 2022)

Countertrend? (August 15, 2022)

Hindsight Capital (April 27, 2022)

One-Sided Markets (September 29, 2021)

End of the Secular Bull? Not So Fast (April 3, 2020)