Jerome Powell and the Federal Reserve spend a lot of time worrying about Inflation Expectations.

They shouldn’t.

Generally, Sentiment Surveys are useless — most of the time — the exception being on rare occasions at the extremes.

They aren’t merely lagging, backward-looking indicators, but instead, inform us as to what the public was experiencing about 3-6 months ago. Typically, it takes people a few weeks or months to subconsciously incorporate broad, subtle changes into their internal mental models, and longer to consciously recognize those nuanced shifts.

Beyond short-term trend extrapolation, inflation expectations have little to no ability to provide insight into the intermediate-future (e.g., 6-12 months) inflation. As to the longer-term, the 5-Year Forward Inflation Expectation Rate are ridonkulously, hilariously, laughably useless. They are so silly as to be “Not even wrong” — just goofy irrelevant guesses.

Here is Brookings explaining the origins of inflation expectations:

“Central bankers’ focus on inflation expectations reflects the emphasis that academic economists, beginning in the late 1960s (including Nobel laureates Edmund Phelps and Milton Friedman), put on inflation expectations as key to the relationship that ties inflation to unemployment.”

So, the pre-globalization, pre-automation, and pre-behavioral finance analog era of the 1970s is the driver of this indicator. This explains in part why it is mostly useless. And yet, despite that, people with important jobs still give it weight. As the nearby charts make clear, they shouldn’t.

We have discussed the problems of forecasting enough in the past that I won’t spend too much time here, other than to point out that humans as a species have no idea what is going to happen in a month or 3, much less 5 years hence.

More specifically, as a group, people get things like inflation expectations precisely backward: Their expectations of inflation are at the very LOWEST right before a spike in inflation is about to occur. As if that wasn’t bad enough, their expectations of inflation are at the very HIGHEST right before inflation peaks and rolls over.

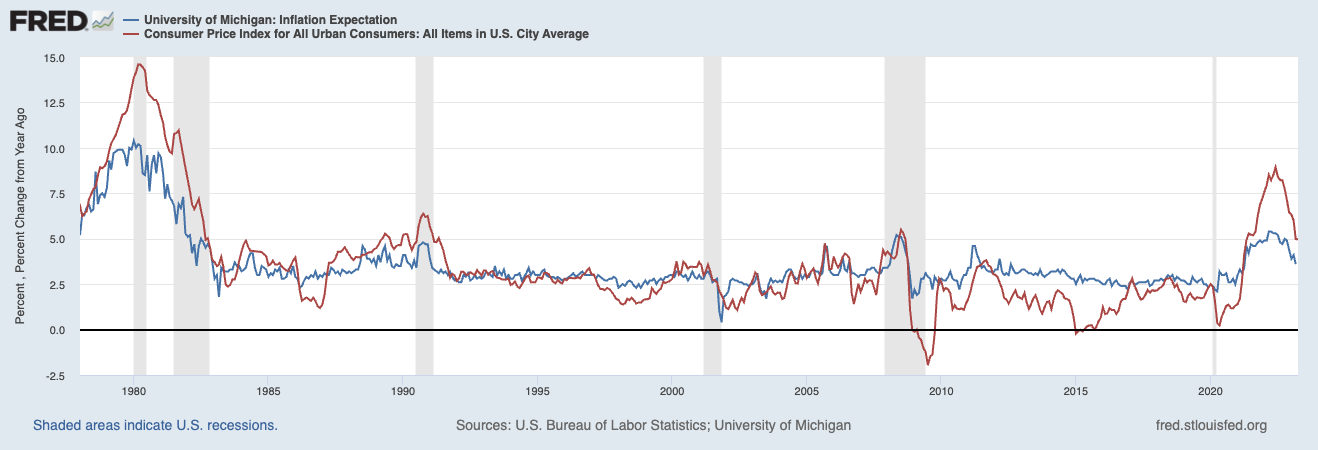

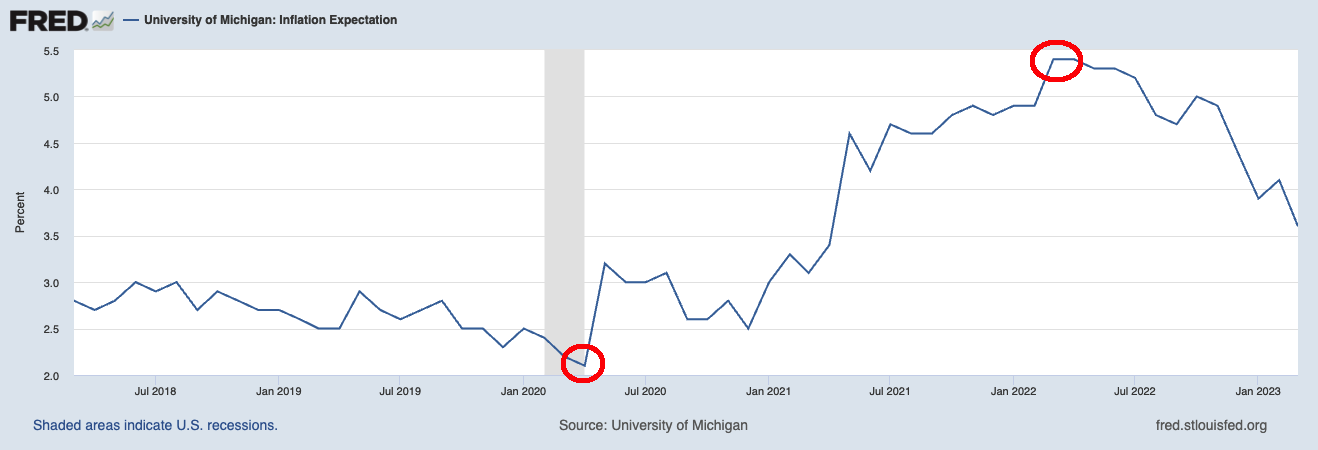

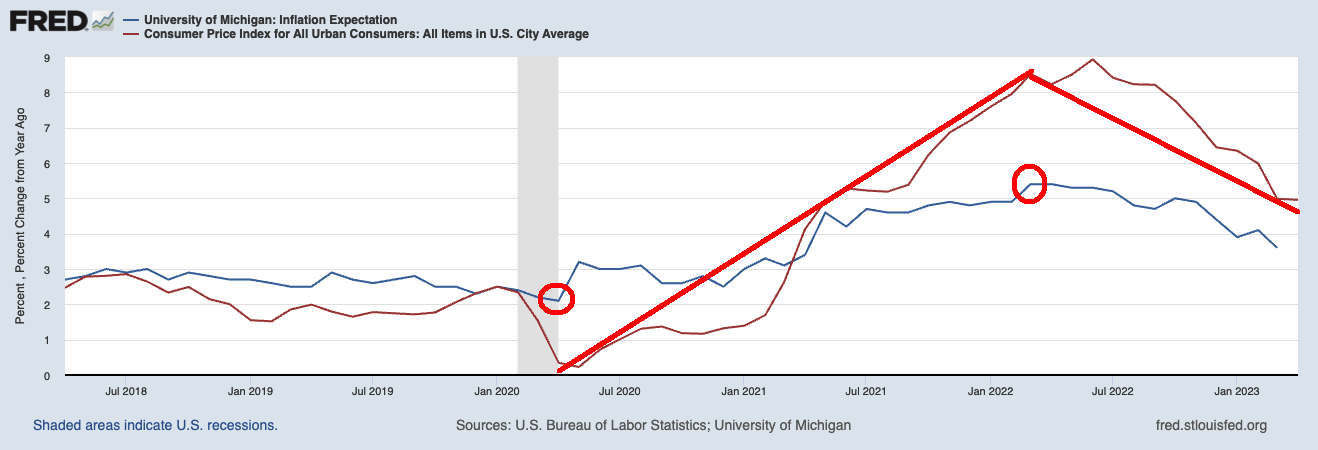

The FRED chart at top shows the high and low of the University of Michigan Inflation Expectations Survey during the pre- and post-pandemic era (2018-2023).

To make this clearer, let’s overlay year-over-year CPI changes1 on Inflation Expectations:

As you can see, expectations bottomed in early 2020, just as CPI began its epic run-up into double digits about a year later.

And as Inflation Expectations plateaued at the peak of inflation data, guess what happened to CPI over the ensuing months?

Annualized inflation:

July 8.52%

Aug 8.26%

Sept 8.20%

Oct 7.75%

Nov 7.11%

Dec 6.45%

Jan 6.41%

Feb 6.04%

March 4.98%

April 4.93%.

As you would expect,2 expectations peaked, just before it began an epic collapse, especially in goods inflation.

Anyone who wants to use Inflation Expectations as an indicator is welcome to — just so long as you recognize that at its extreme readings, it works best as a CONTRARY INDICATOR…

UPDATE: May 17, 2023

We are directed to a recent Fed paper that makes the same point but from a different perspective:

“Economists and economic policymakers believe that households’ and firms’ expectations of future inflation are a key determinant of actual inflation. A review of the relevant theoretical and empirical literature suggests that this belief rests on extremely shaky foundations, and a case is made that adhering to it uncritically could easily lead to serious policy errors.”

See also:

Why Do We Think That Inflation Expectations Matter for Inflation? (And Should We?)

Jeremy B. Rudd

Federal Reserve Board* September 23, 2021.

Previously:

2000: “No matter how you cut it, you’ve got to own Cisco” (May 15, 2023)

Can Anyone Catch Nokia? (October 26, 2022)

Gradually, Then Suddenly (October 1, 2021).

Why the Apple Store Will Fail (May 20, 2021)

Nobody Knows Nuthin’ (May 5, 2016)

How News Looks When Its Old (October 29, 2021)

__________

1. Because the CPI swing is so large, it compresses expectations) makes the expectations portion appear compressed

2. That list is via my colleague Ben Carlson