Jill on Money: The Big Picture with Barry Ritholtz

On this episode of Jill on Money, Jill sits down with the blogfather himself, Barry Ritholtz! Find out how Barry got...

Exciting news! In a few weeks, we are heading down to Naples, Florida, where we just launched a new office! Everybody knows...

Exciting news! In a few weeks, we are heading down to Naples, Florida, where we just launched a new office! Everybody knows...

As promised, here is my presentation “Navigating Financial Disasters” from today at the Orlando Money Show…

As promised, here is my presentation “Navigating Financial Disasters” from today at the Orlando Money Show…

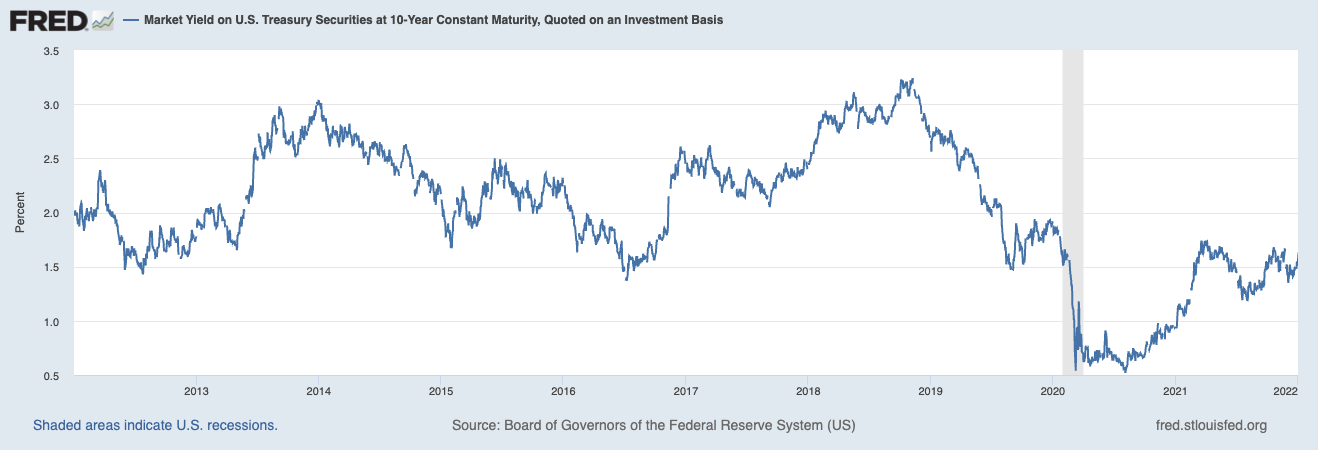

Since the Great Financial Crisis in 2008-09, the income portion of portfolios has been almost an afterthought. Your...

Since the Great Financial Crisis in 2008-09, the income portion of portfolios has been almost an afterthought. Your...

Exciting news! I am heading to Charlotte next month, and I will be bringing a full complement of the crew with me! We will be...

Exciting news! I am heading to Charlotte next month, and I will be bringing a full complement of the crew with me! We will be...

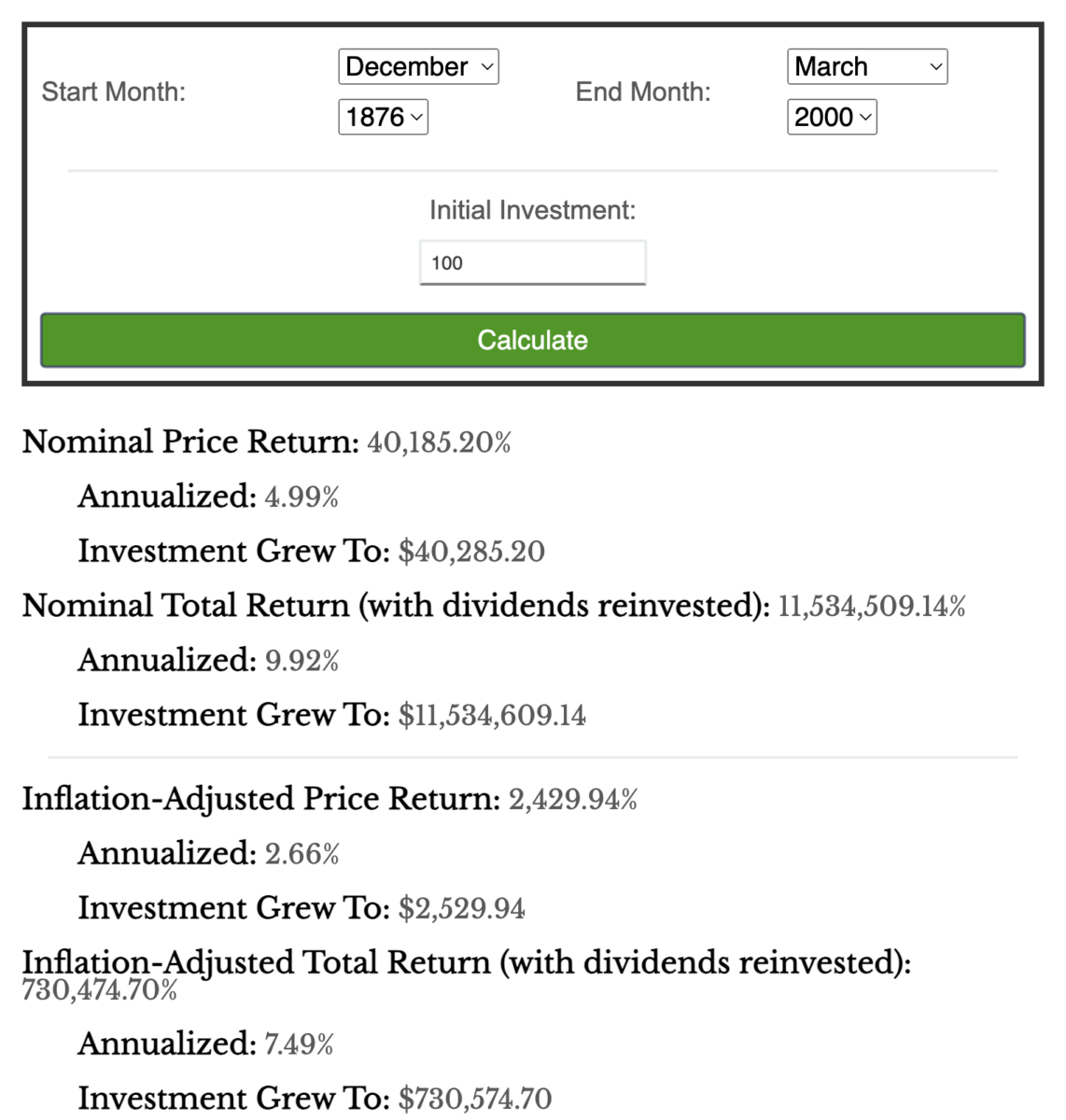

I have been playing with Nick’s S&P 500 calculator, and it’s pretty damned, cool. He used data from Robert...

I have been playing with Nick’s S&P 500 calculator, and it’s pretty damned, cool. He used data from Robert...

“This is the last straw, I am quitting today.” I was in Newport Beach at a PIMCO-sponsored event where I presented on...

“This is the last straw, I am quitting today.” I was in Newport Beach at a PIMCO-sponsored event where I presented on...

I made it back home from California late last night after a long day of travel and an exhausting but absolutely exhilarating week....

I made it back home from California late last night after a long day of travel and an exhausting but absolutely exhilarating week....

Future Proof 2023 kicked off yesterday, and it was everything we were hoping it would be. After overnight drizzle, the weather...

Future Proof 2023 kicked off yesterday, and it was everything we were hoping it would be. After overnight drizzle, the weather...

We hosted the 1st Future Proof conference last year, and it was a banger! (full reviews here). This year, we are upping the...

We hosted the 1st Future Proof conference last year, and it was a banger! (full reviews here). This year, we are upping the...

Get subscriber-only insights and news delivered by Barry every two weeks.