As we have been discussing since May of this year, there are increasing signs we have been groping for a bottom in the equity markets. This “Process” is not a single event but rather, a series of events the totality of which increasingly weighs the probability towards that positive resolution.

I use the word probability because this outcome is not pre-ordained, but rather, subject to future events which have yet to unfold. When investors look forward, we (collectively) make probabilistic bets as to the odds of events occurring and the impact of those future events once they do occur. Some are known and already priced in, more are ambiguous, not fully reflected in market prices, and some are random surprises that by definition markets have not accounted for.

Hence, I have caveats.

My thinking is any bottoming process is partially dependent on future FOMC actions. I have been fairly vocal that inflation has peaked, the Fed has already overtightened, and they run the risk of doing too much economic damage fighting a demon that has already been exorcised.

But my job is not to give the Fed policy advice, it is instead to provide clients with insight and investment advice. The best way I can accomplish that is to recognize the ambiguities created by none of us knowing if the FOMC will be very right, a little wrong or very wrong. Those three options will determine whether or not the equity and bond markets make a bottom now, at some point in 2023, or at some future date beyond.

My take on these probabilities looks something like this:

1. The Fed gets it precisely right: Yay! Inflation is vanquished, the economy makes a soft landing, rainbows and sprinkles and unicorns! Inflation comes down to 2-3%, Unemployment never goes above 4%, and GDP stays around 2%. It’s Goldilocks as far as the eye can see. It’s nothing but 10% gains a year forever — all hail the U.S. central bank! (20% chance)

2. The Fed gets it a little wrong: The Fed takes rates over 5% and keeps them there way too long. Parts of the economy suffer – notably residential real estate, new job creation, and consumer spending. U3 unemployment goes from its current 3.7% to closer to 5%. New job creation falls to under 100k per month. GDP is flattish to slightly positive. Given these headwinds, the overall economy remains fairly resilient, with falling savings rates and a lack of wage gains offset by falling inflation. Maybe this economic slowing results in a mild shallow recession, maybe not. Markets go sideways through Q1 perhaps even into Q2, then take off. (50% chance)

3. The Fed totally blows it: The Fed tightens and keeps tightening, straight through 5% towards 6%. Ignoring the deflation in goods and focusing on the inflation in services, especially ren (which they are causing) they stay too tight for too long. GDP goes negative, Unemployment goes above 5-6%, house prices fall 10-15%, and Consumer spending crashes. (30% chance)

If the Fed was the only game in town, our task would be easier. But I do not assume that the Federal Reserve is the only significant market input or economic factor. Investors need to recognize:

The economy has thus far remained resilient;

Corporate Profits have remained robust;

Consumers are still spending;

Households and corporate balance sheets are healthy;

Valuations have become more attractive;

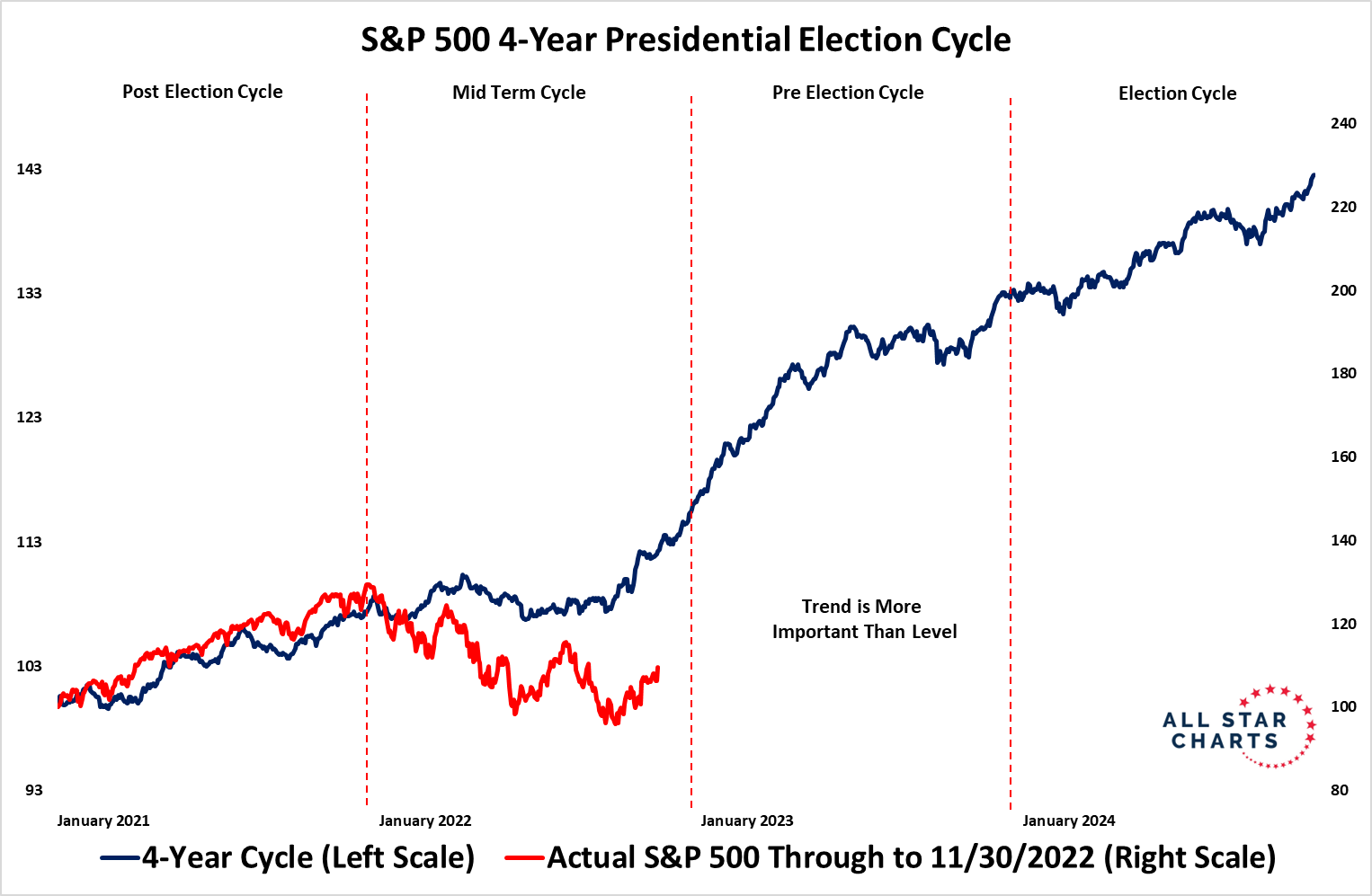

Seasonal patterns are positive (see chart above via JC).

This is why I put a 50% probability of markets finding a bottom sometime between October 2022 and March 2023.

If you are a long-term investor, I would suggest considering Value and Small Caps. Financials have held up well also, as they generate better profits when rates are not at zero. And I never like to bet against tech, especially after it has fallen substantially. I would be more cautious with single stock risk, specifically, those circumstances where there are problematic business models, mercurial CEOs, and/or increased competition.

I acknowledge there are lots of ways all of the above can go south. I remain — hopeful? Constructive? Engaging in wishful thinking? Perhaps all three.

YMMV.

UPDATE 2: December 3, 2022:

I see Claudia Sahm — creator of the Sahm rule — sees the world similarly:

Burden of proof is on the inflation hawks now Reality shows a “soft landing” in 2023 in the United States taking shape. We avoid a recession, we keep the job-full recovery, and inflation moves back down. Hawks, it’s time to join us in reality.

UPDATE: December 2, 2022:

NFP payroll comes in hot at 263k, which is consistent with the resilient economy thesis (middle choice)

See also:

Jerome Powell Signals Fed Prepared to Slow Rate-Rise Pace in December (November 30, 2022)

U.S. gas prices plunge toward $3 a gallon as demand drops worldwide (November 30, 2022)

Previously:

Big Moves: Bears & Bottoms (November 11, 2022)

Groping for a Bottom (October 14, 2022)

7th Inning Stretch (September 30, 2022)

Countertrend? (August 15, 2022)

Big Up Big Down Days (May 5, 2022)

Too Many Bears (May 3, 2022)

End of the Secular Bull? Not So Fast (April 3, 2020)